Filing Customs Declarations Using Customs Declarations UK

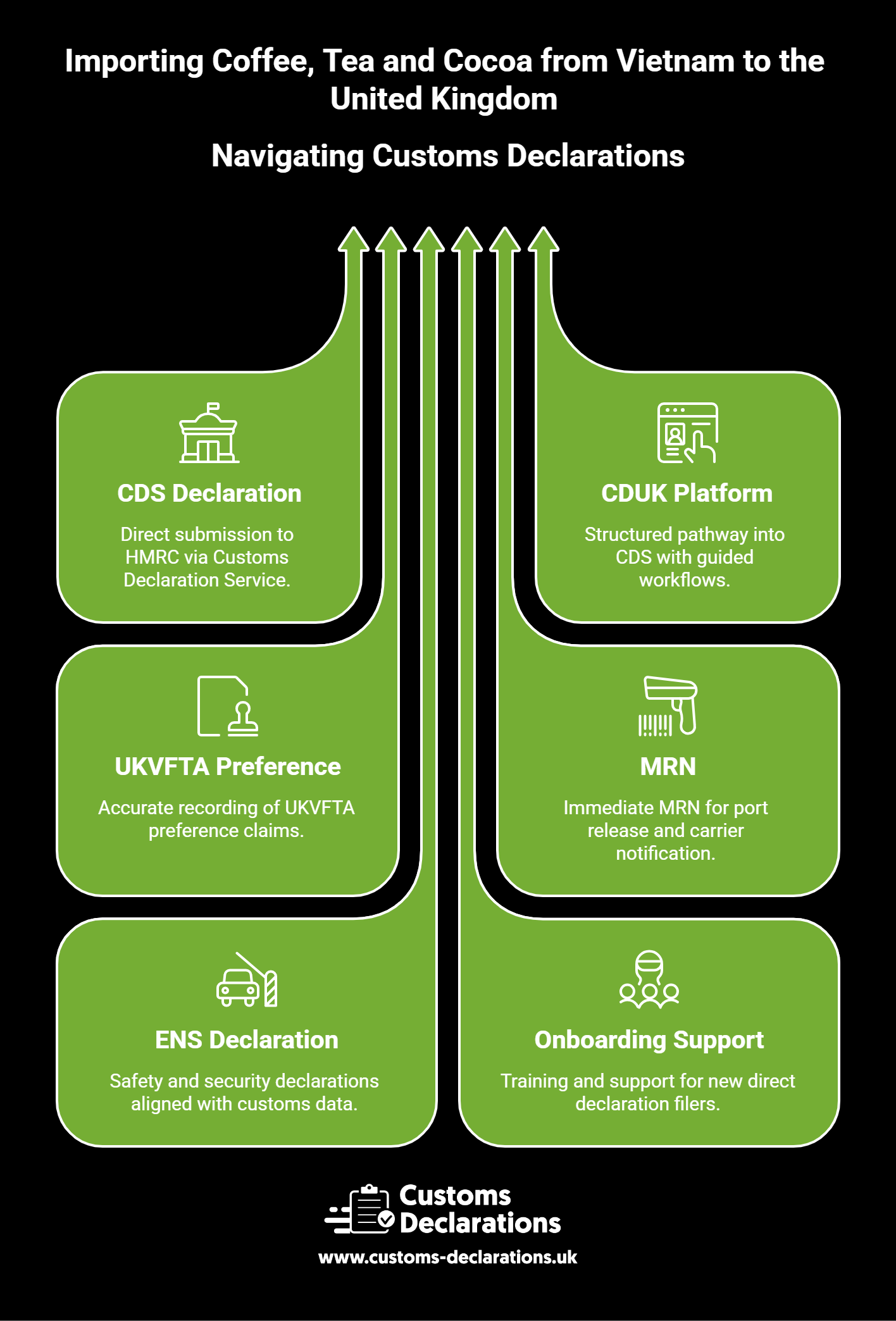

At the heart of every compliant UK import is a correctly filed CDS declaration — submitted to HMRC through the Customs Declaration Service (CDS). The Customs Declarations UK (CDUK) platform provides importers with a structured, validated pathway into CDS, removing much of the complexity from the declaration process.

Using CDUK, importers of coffee, tea, and cocoa from Vietnam can:

Prepare and submit full import declarations directly to HMRC’s CDS through guided, plain-English workflows that prompt for all required data elements — importer and exporter identity, commodity code, customs value, Incoterms, country of origin, and preference claim details. The platform’s real-time validation engine checks for missing or inconsistent data before transmission, catching errors that would otherwise result in rejection or post-clearance HMRC queries.

Record the UKVFTA preference claim accurately, including the basis for that claim (Statement on Origin or importer’s knowledge) and the associated documentary reference. This creates an audit-ready record that can be produced promptly if HMRC requests verification.

Receive the Movement Reference Number (MRN) immediately upon HMRC acceptance, which serves as the gateway notification for port release and must be provided to the carrier and port Community System Provider (CSP).

In addition to import declarations, CDUK supports the filing of ENS declarations — Entry Summary Declarations required for safety and security purposes on goods arriving into the UK. These must be aligned with the customs declaration in terms of goods description, weights, and consignee details. Mismatches between ENS and customs data are a frequent and avoidable cause of border holds. CDUK’s integration with leading Community System Providers — CNS, MCP, and CCS-UK — helps ensure seamless data flow across the port and HMRC systems.

For businesses new to direct declaration filing, CDUK offers onboarding support and training, enabling importers to manage their customs filings in-house and reduce dependence on third-party brokers. The platform’s pay-as-you-go pricing model, with declarations available from £4, makes it commercially accessible even for lower-volume importers.