HMRC and HM Treasury recently jointly published “Modernising the UK Customs Regime,” a call for evidence asking a question with real implications for every importer, exporter, and intermediary in the country: is the UK’s declaration-based customs model still fit for a trading world that runs increasingly on structured digital data? The call for evidence is open for twelve weeks, closing on 15 September 2026, and is led jointly by HMRC’s R Holt and HM Treasury’s T Smiles.

Why now

The foreword, signed by Dan Tomlinson MP, Exchequer Secretary to the Treasury, frames this as the next chapter after several years of foundation-building. Since EU Exit, HMRC has stood up the Customs Declaration Service — which cleared over 91 million customs declarations into and out of the UK in 2025 — alongside the Goods Vehicle Movement Service, and has delivered the customs aspects of the Windsor Framework for Northern Ireland. Having established that foundation, the government is now turning its attention to whether the underlying model of customs — declarations submitted at a single point in a goods movement — still matches how modern, digitally-enabled supply chains actually operate.

Notably, this call for evidence was published the same day as HMRC’s separate consultation on mandatory registration for customs intermediaries, and the two are explicitly linked: HMRC encourages respondents interested in one to also engage with the other, since both speak to the future shape of the customs and intermediary landscape.

The future of trade: a digitalising world

The call for evidence opens by setting out just how far trade digitalisation has already progressed. The UK’s own Electronic Trade Documents Act 2023 gave electronic trade documents, such as Bills of Lading and air waybills, the same legal standing as their paper equivalents — a change estimated to deliver a net benefit of around £1.14 billion to the UK economy over a decade through reduced administrative costs. Internationally, major container shipping carriers have committed to 100% adoption of electronic Bills of Lading by 2030, and a 2024 industry survey found that roughly half of supply chain participants already use electronic Bills of Lading in some capacity.

Other customs authorities are moving in parallel. The EU’s Customs Union reform programme sets out plans to replace traditional declarations with data flowing directly from digitalised trade systems, alongside more advanced AI-enabled risk assessment. US Customs and Border Protection is continuing to modernise its own centralised import/export platform, with a particular focus on interoperability and trusted data sharing across supply chains. HMRC wants to understand how UK businesses are experiencing this shift already, how they expect their own trade operations to change over the next decade, and how the UK’s approach compares with what traders see in other jurisdictions.

AI, Electronic Trade Documents and Supply-Chain Data: HMRC’s Vision for the Future Border

The heart of the call for evidence — and arguably its most consequential chapter — asks whether HMRC’s data model itself needs to change. The current approach relies heavily on information submitted through a customs declaration at a specific point in a goods movement. HMRC notes that previous UK border technology pilots have already shown that most customs risking data requirements could, in principle, be met using Electronic Trade Documents and other data drawn directly from digital trade and inventory systems, rather than being separately keyed into a declaration.

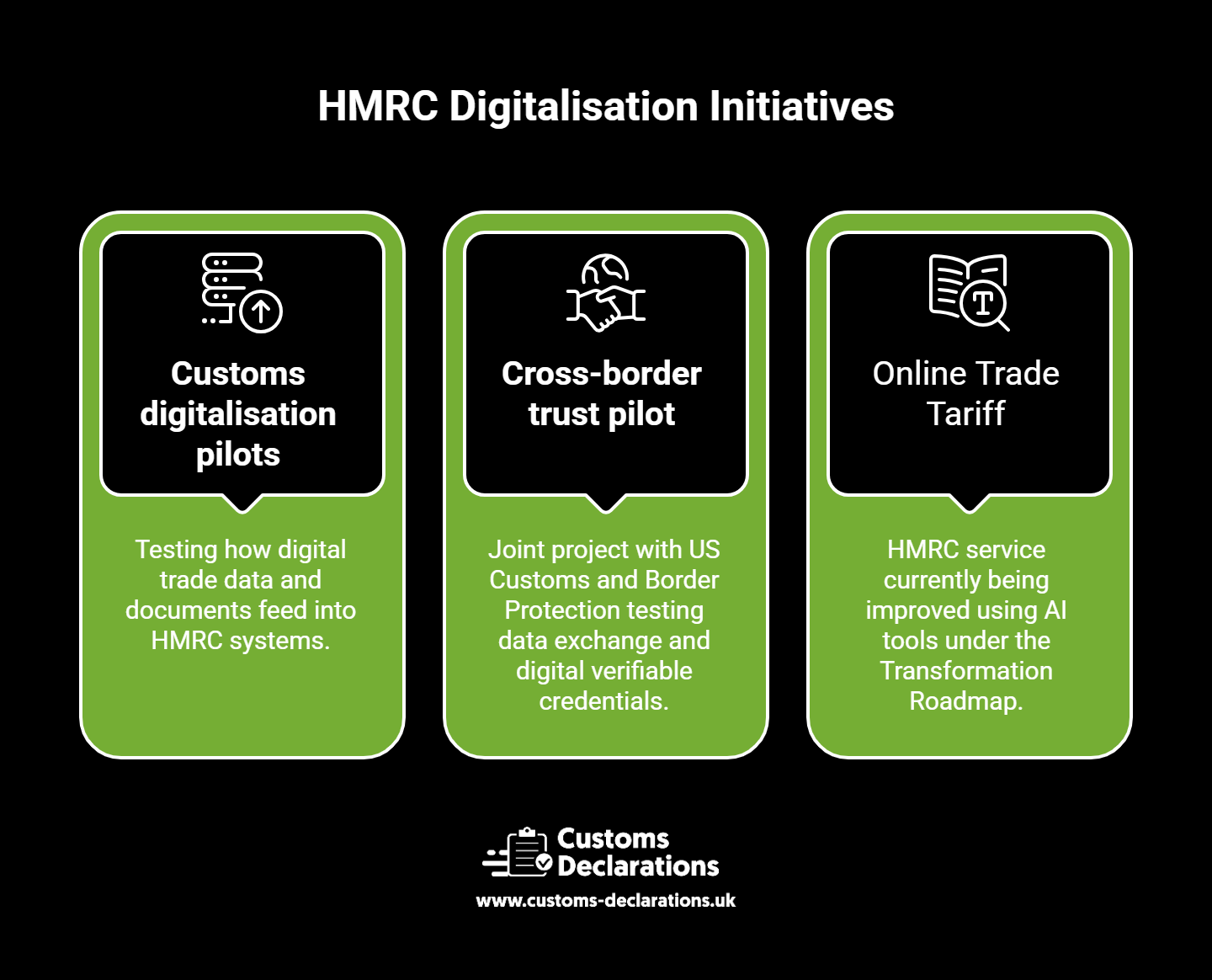

This is where artificial intelligence enters the picture directly. HMRC points to work already under way: at Tax Update 2025, two customs digitalisation pilots were announced, one testing how digital trade data and documents could feed into HMRC systems, and a second, run jointly with US Customs and Border Protection, testing data exchange and digital verifiable credentials as a way of building cross-border trust. Separately, under its Transformation Roadmap, HMRC has begun using AI tools to improve its Online Trade Tariff service. The call for evidence asks whether supply chain data — shipment records, inventory systems, commercial documents — should play a limited role alongside existing declarations, a more significant supporting role, or eventually a primary one. It also probes practical questions of interoperability: whether businesses are familiar with digital data-sharing frameworks such as UN/CEFACT, Peppol or TradeTrust, where data compatibility issues most commonly arise, and how a shift toward supply-chain-derived data might change the working relationship between traders and the customs intermediaries — brokers, freight forwarders, and software providers — who currently handle the great majority of UK declarations.

The future of trust and authorisations

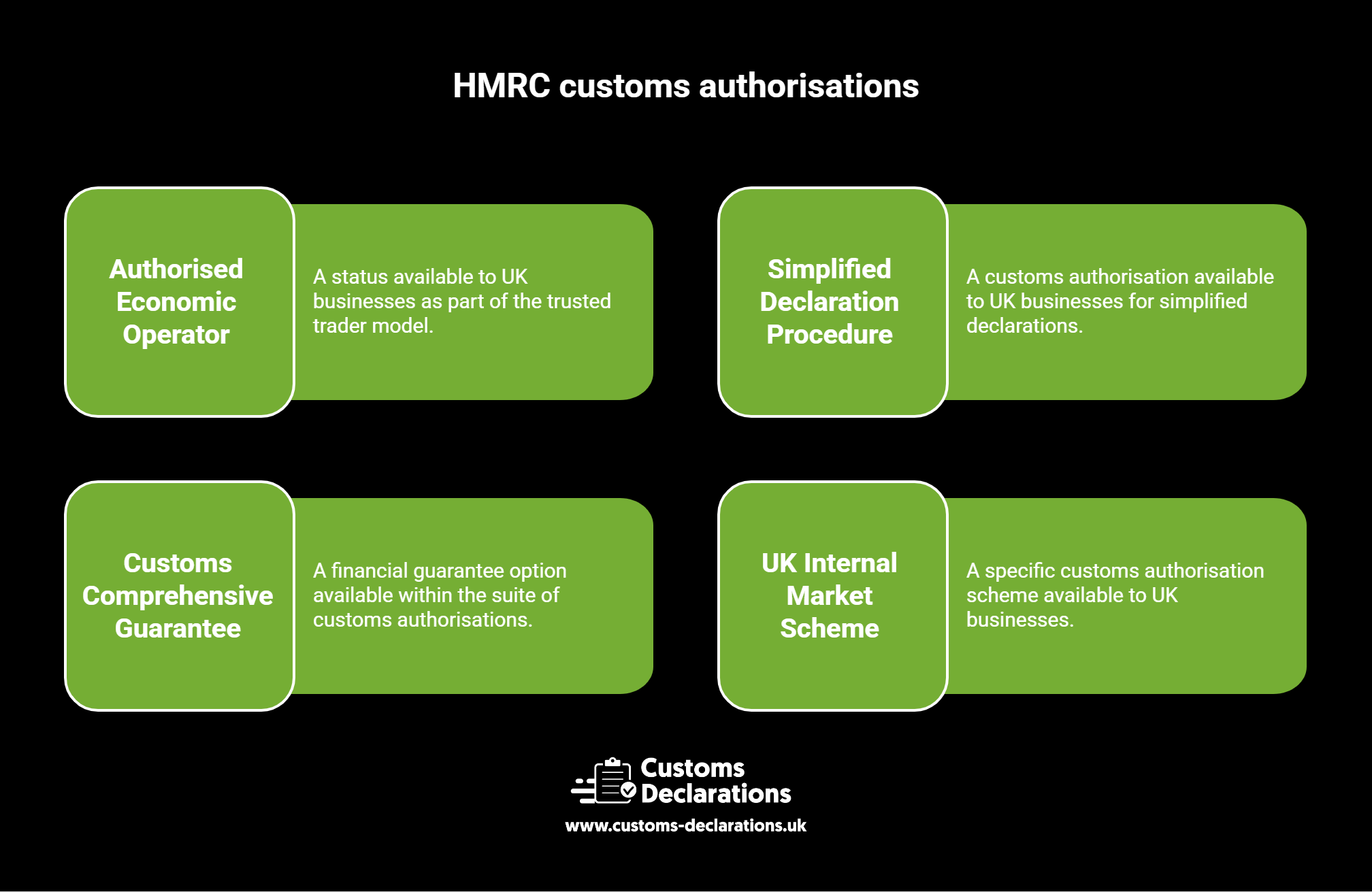

The third strand examines HMRC’s “trusted trader model” — the full suite of customs authorisations available to UK businesses, including Authorised Economic Operator (AEO) status, Simplified Declaration Procedure, Customs Comprehensive Guarantee, and the UK Internal Market Scheme, among many others. Unlike some other customs administrations, the UK does not mandate that traders hold any particular authorisation, or treat AEO status as a prerequisite for accessing further simplifications; businesses currently choose the authorisations that suit them. HMRC wants views on whether that flexible, decentralised approach still serves businesses well as trade becomes more data-driven, whether authorisations are easy to apply for and maintain in practice, and whether alternative models — potentially more tailored to different business types, or more closely aligned with trusted trader models used elsewhere — should be explored.

Who should respond, and how

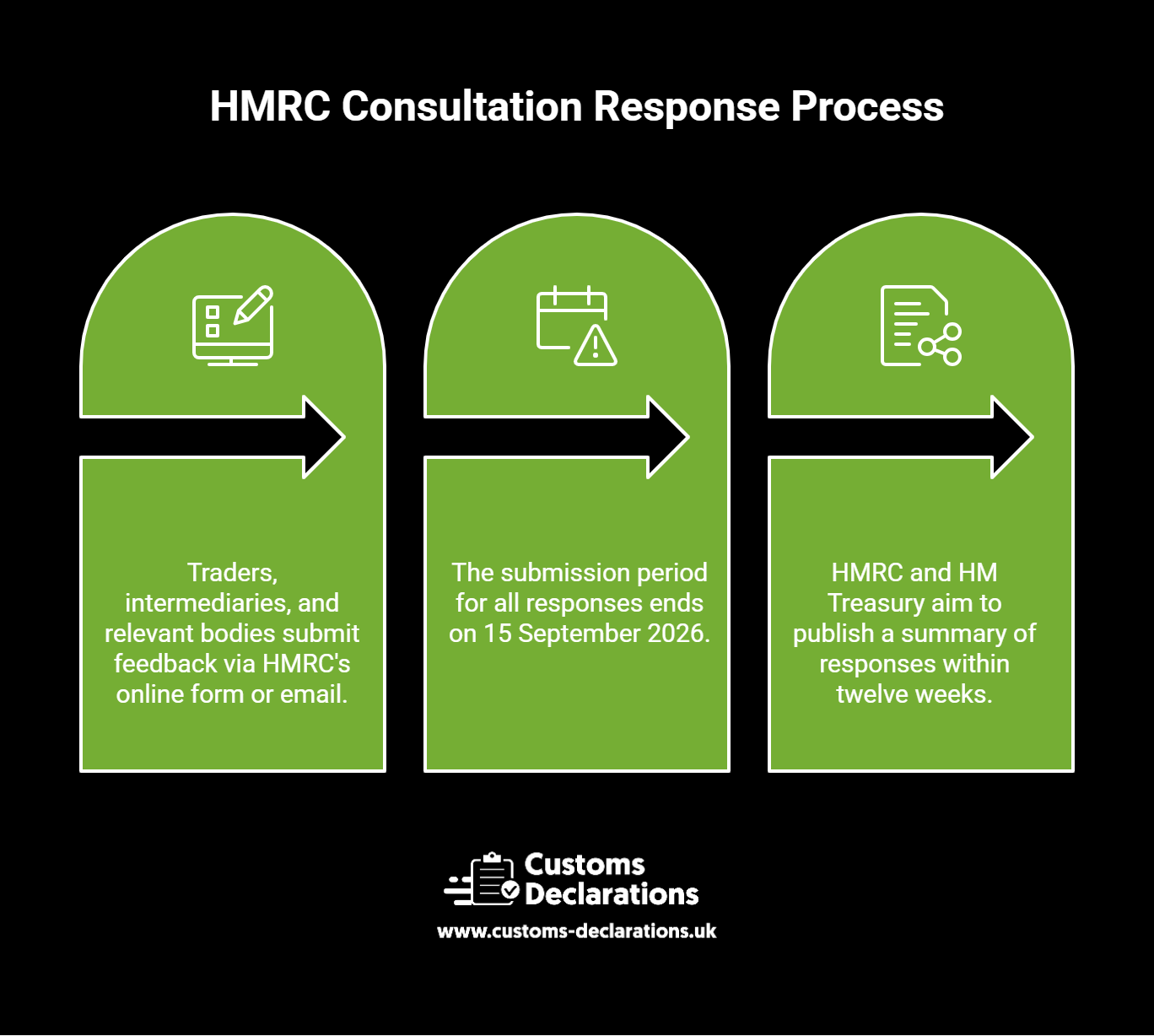

HMRC has been explicit that it wants to hear from businesses at every stage of digital maturity, not only those already running sophisticated digital trade operations. Traders, customs intermediaries, freight forwarders, hauliers, customs software providers, and representative or trade bodies are all named as key audiences, including organisations that do not currently trade internationally but might in future. Responses are encouraged via HMRC’s online form, though email responses are also accepted for those unable to use it, and partial responses focused on the sections most relevant to a given respondent are explicitly welcomed. The window closes on 15 September 2026, after which HMRC and HM Treasury aim to publish a summary of responses within twelve weeks.

Why this matters for CDUK’s audience

For traders, intermediaries, and software providers alike, this call for evidence is a signal that HMRC is seriously weighing a shift from a purely declaration-based model toward one that draws more directly on supply-chain and commercial data — with AI playing a growing role in risk assessment and document processing along the way. At Customs Declarations UK, our guided wizard workflows and AI-powered document extraction already point in this direction, helping traders and intermediaries structure and validate their data before it ever reaches HMRC. As this review develops, we will continue to track how it might reshape declaration requirements, data standards, and the intermediary relationship, and will keep our platform aligned with wherever the UK customs regime ultimately lands.