HMRC has opened a new consultation proposing mandatory registration for customs intermediaries — the agents, brokers, freight forwarders, and express operators who submit customs declarations on behalf of traders. Published on 23 June 2026 under the title “Customs intermediaries: introduction of Mandatory Registration,” the consultation runs for thirteen weeks, closing on 21 September 2026, and signals one of the more significant shifts in how the customs intermediary sector could be governed since the end of the Brexit transition period

Why HMRC is acting now

The rationale set out by HMRC centres on a simple imbalance: traders overwhelmingly depend on intermediaries to meet their customs obligations, yet there is currently no minimum bar an intermediary must clear to operate. HMRC cites its own trade statistics showing that the large majority of international customs declarations cleared in 2025 were handled by a third party, with the great majority of traders relying solely on an intermediary to declare all of their trade. Against that backdrop, the government argues that a lack of barriers to entry sits awkwardly with the expectation that intermediaries acting on behalf of traders should themselves be compliant operators.

This is not HMRC’s first move in this direction. A February 2022 call for evidence, “An Independent Customs Regime,” first raised questions about the intermediary sector, followed by a June 2023 consultation on introducing a Voluntary Standard for customs intermediaries. That work matured into an actual Standard, developed jointly with industry and the British Standards Institution, published on 3 June 2026. The new mandatory registration consultation is presented as the next logical step: building on the Standard by giving it teeth through a registration gateway, rather than relying on voluntary adoption alone.

HMRC also draws a direct parallel with tax advisers. In November 2025, the government introduced a legal requirement for tax advisers who deal with HMRC on a client’s behalf to register and meet minimum standards from May 2026. Customs intermediaries were explicitly carved out of that requirement at the time — this consultation proposes bringing them into a comparable framework, so that customs and tax are governed by a consistent registration approach.

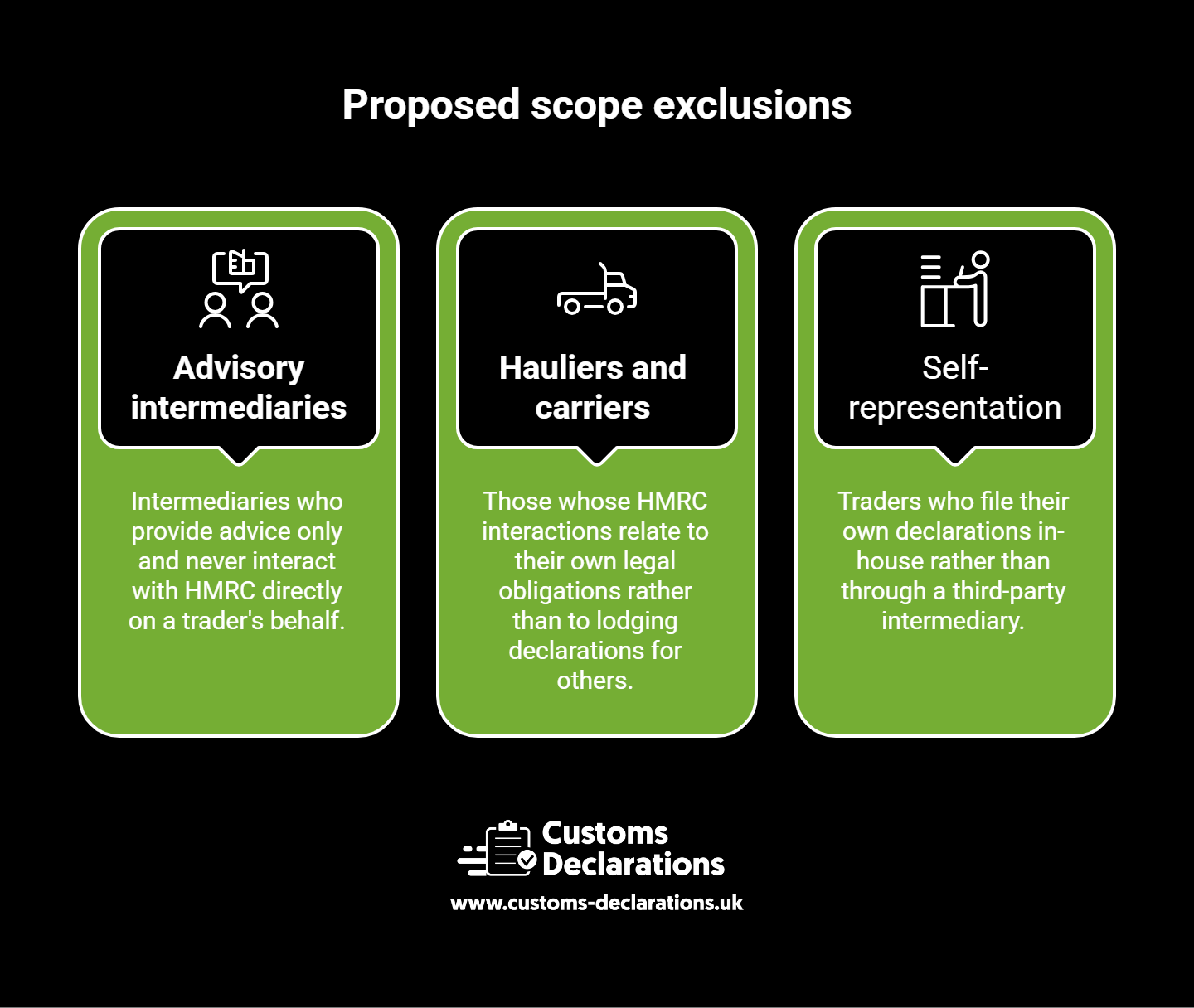

Proposed scope

HMRC’s proposal would apply mandatory registration UK-wide, covering both import and export activity, and consistently across all types of customs declaration rather than being confined to a specific regime. Three categories are proposed as out of scope: intermediaries who provide advice only and never interact with HMRC directly on a trader’s behalf; hauliers and carriers, whose HMRC interactions relate to their own legal obligations rather than to lodging declarations for others; and, notably, self-representation. Traders who file their own declarations in-house — rather than through a third-party intermediary — would not be brought within the registration requirement, since the stated aim is to target intermediary-specific harm rather than add burdens for traders managing their own filings.

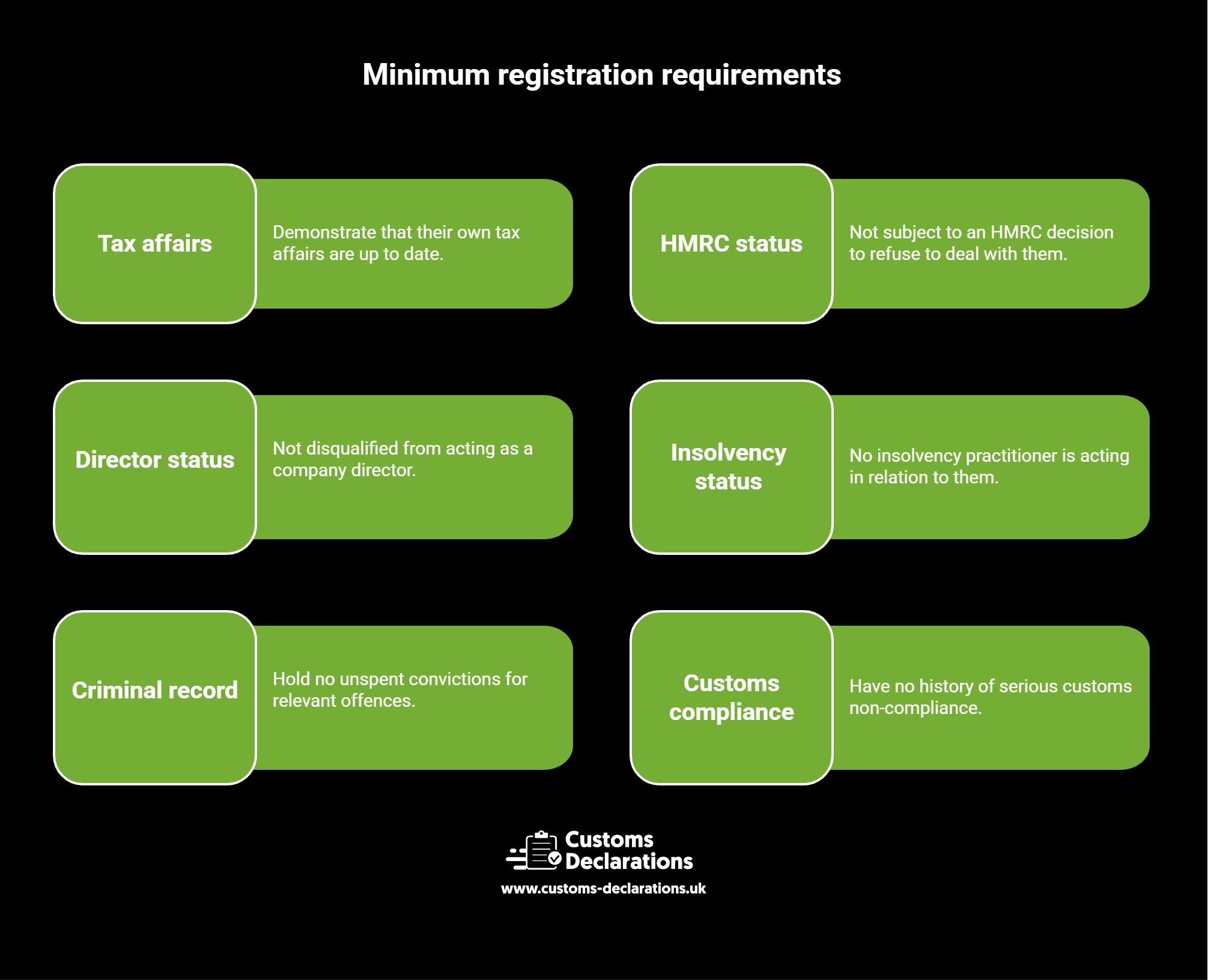

The proposed minimum requirements

The consultation proposes that registration would be conditional on a small set of checks, deliberately modelled on the May 2026 tax adviser requirements to keep the approach proportionate and consistent. An intermediary would need to demonstrate that their own tax affairs are up to date, that they are not subject to an HMRC decision to refuse to deal with them, that they are not disqualified from acting as a company director, that no insolvency practitioner is acting in relation to them, that they hold no unspent convictions for relevant offences, and that they have no history of serious customs non-compliance. HMRC proposes to run automated checks both at the point of registration and periodically thereafter.

Enforcement: a graduated model

Rather than an all-or-nothing sanction, HMRC is proposing a graduated enforcement approach mirroring the tax adviser regime. Registration would become a prerequisite for interacting with HMRC’s systems, with ongoing compliance monitored on a risk basis. Where issues arise, the proposed sequence runs from early engagement and warnings, through temporary suspension where problems are not resolved, to staged escalation toward financial penalties for persistent or serious non-compliance — with removal or restriction of an intermediary’s ability to submit declarations reserved as a last resort. HMRC states this would sit alongside guidance, opportunities to remediate, and rights of review and appeal.

Timeline and how to respond

The consultation is open until 21 September 2026, with responses invited by email to HMRC’s Customs Intermediaries Policy Team. HMRC has indicated it will run webinars for interested parties during the consultation window, and intends to publish a summary of responses once the consultation closes, followed by further decisions on legislation and implementation.

What this means for the trade

For traders who currently rely on intermediaries, mandatory registration is designed to offer a clearer baseline of assurance about who they are dealing with. For intermediaries themselves, the direction of travel is worth acting on early — reviewing tax compliance status, directorship history, and any prior customs compliance issues well ahead of any transitional period HMRC ultimately sets. For businesses that already file their own declarations in-house, the proposed exclusion of self-representation from scope is a useful point of clarity: it confirms that direct, self-managed filing sits outside the registration requirement being proposed here.

Source: HMRC, “Customs intermediaries: introduction of Mandatory Registration,” GOV.UK https://www.gov.uk/government/consultations/introduction-of-mandatory-registration-for-customs-intermediaries/customs-intermediaries-introduction-of-mandatory-registration