The European Union has taken one of the most consequential steps in customs policy in a generation. From 1 July 2026, the long-standing duty-free treatment of low-value parcels entering the EU has ended. In its place, a flat customs duty of €3 per item applies to consignments with an intrinsic value of €150 or less. For importers, exporters, freight forwarders, and e-commerce operators — including those accessing European markets from the UK — this is not a marginal adjustment. It is a structural shift in how cross-border trade flows into the world’s largest single market.

This article sets out what has changed, why it changed, how the new duty works in practice, and what it means for businesses operating in or trading with the EU.

The End of the De Minimis Exemption

For decades, goods arriving in the EU in low-value consignments were exempt from customs duty. The threshold — goods with an intrinsic value of €150 or less — was originally established to spare customs authorities from processing volumes of small parcels where the administrative cost of collection would outweigh the revenue generated. When introduced, this was a sound rationale. The logistics of international parcel trade were simply not capable of delivering billions of individual shipments to doorsteps across the EU.

The digitalisation of customs procedures has fundamentally changed that picture. Electronic data is now available for every imported good, meaning the original administrative justification for the exemption is no longer valid. At the same time, the volume of low-value parcels has grown to a scale that makes the exemption commercially and fiscally unsustainable.

According to the European Commission, almost 5.9 billion low-value items were directly shipped from third countries to consumers in the EU in 2025 alone, without paying customs duties. That is roughly 12 million parcels a day and twice the number recorded the year before. The figure stood at just 1.4 billion in 2022.

The reform is also a response to a documented compliance failure. Targeted inspections carried out across the EU throughout 2025 in cosmetics, personal protective equipment, food supplements, toys, and electronics revealed alarming non-compliance: over 60 percent of checked products failed EU standards due to missing labels, forbidden ingredients, or absent safety documentation. The duty-free regime had, in effect, created a channel through which non-compliant goods could enter the EU market at scale, undermining both consumer protection and fair competition for EU-based sellers.

The Council of the EU acted on 12 December 2025, agreeing a coordinated response. Today’s move followed the Council’s commitment in November 2025 to work towards a simple, temporary solution to levy customs duties on such goods as soon as possible in 2026.

The Legal Basis and Regulatory Architecture

The new €3 flat-rate duty is established under Council Regulation (EU) 2026/382, which was formally agreed by the Council of the European Union on 11 February 2026. The measure applies from 1 July 2026 until 1 July 2028.

To ensure the practical implementation of the new legislation, the UCC Delegated Act and Implementing Act had to be amended. The Commission adopted the delegated rules on 30 April 2026, which are now under scrutiny, and the implementing rules were published in the Official Journal of the EU on 8 June 2026.

The 2028 end date is not arbitrary. The temporary €3 customs duty applies until 1 July 2028, after which normal customs duties will apply depending on the type of good. The Customs Data Hub for e-commerce is expected to come online at that point, enabling full tariff treatment based on each product’s classification. The €3 duty is therefore explicitly an interim measure: it bridges the gap between the collapse of the de minimis regime and the deployment of a permanent digital customs infrastructure.

How the Duty Works in Practice

What is Covered

The duty applies to all goods in consignments up to €150 sold in distance sales, such as online purchases from non-EU suppliers, regardless of which VAT scheme is used — whether IOSS, Special Arrangements, or standard VAT.

It is important to understand what “intrinsic value” means for the purposes of the €150 threshold. Intrinsic value means the price of the goods themselves and nothing else — it does not include shipping or transport costs, insurance, or any other taxes, duties, or fees, as long as those are shown separately on the invoice. A product priced at €140 with €20 shipping therefore has an intrinsic value of €140, not €160, and remains within the €150 threshold.

Per Item, Not Per Parcel

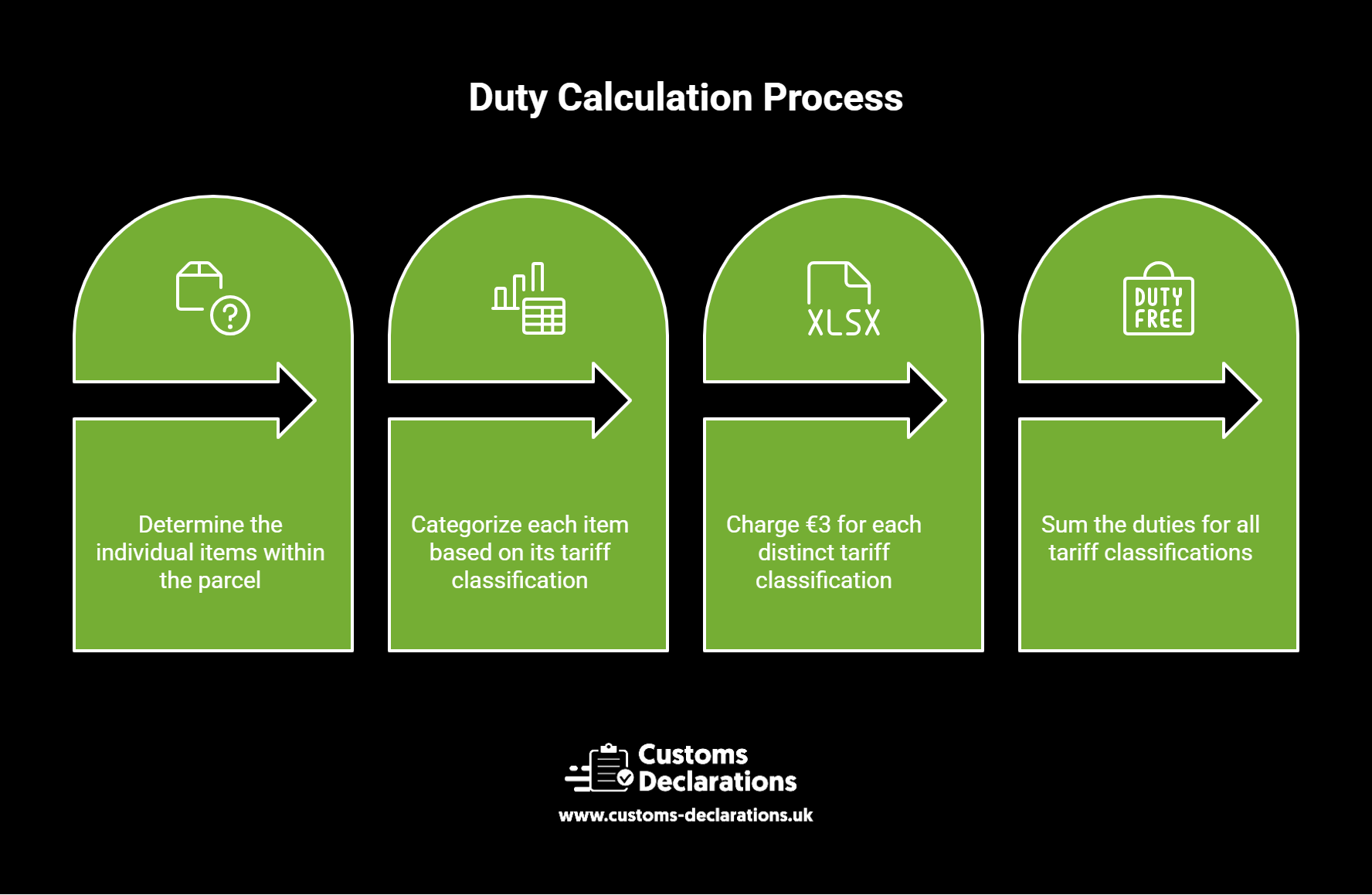

A critical feature of the new duty is how it is calculated. The duty applies per item in a consignment, based on tariff classification rather than quantity. This means a single parcel containing goods classified under multiple HS codes will attract multiple €3 charges.

As the European Commission’s own guidance illustrates: a parcel containing one blouse made of silk and two blouses made of wool contains two distinct items by tariff sub-heading, and €6 in customs duty is due — not €3. By contrast, three blouses of the same material would fall under a single tariff heading and attract a single €3 charge, regardless of quantity.

A further practical example from the European Commission’s guidance: a parcel containing a smartphone, a charger, and earphones attracts three separate €3 charges, one for each distinct tariff heading, resulting in €9 of duty on a single consignment.

Who Bears the Duty

The €3 rate is applied to all goods entering the EU for which non-EU sellers are registered in the EU’s Import One-Stop Shop (IOSS) for VAT purposes. This encompasses an estimated 93% of all e-commerce flows to the EU. The Commission has indicated it will monitor whether traders divert flows away from IOSS to circumvent the duty, and from 1 October 2026, the Commission must conduct monthly monitoring to determine whether such diversion is occurring. Where evidence is found, it may propose extending the duty to all low-value imports, including those not registered under IOSS.

What is Excluded

Not all low-value goods fall within scope. Goods benefiting from preferential treatment under free trade agreements or customs union measures can retain their preferential duty rate, but only if VAT has not been collected through IOSS and the goods are declared using the standard H1 customs declaration. This creates an important asymmetry: FTA-originating goods submitted through IOSS will default to the €3 flat rate rather than the lower preferential rate. Sellers and logistics providers managing preferential-origin goods should confirm which declaration pathway their shipments use before assuming FTA savings apply.

Business-to-business imports to VAT-registered recipients are also treated differently, with standard duty rates applying rather than the €3 flat charge.

VAT and the €3 Duty: An Important Distinction

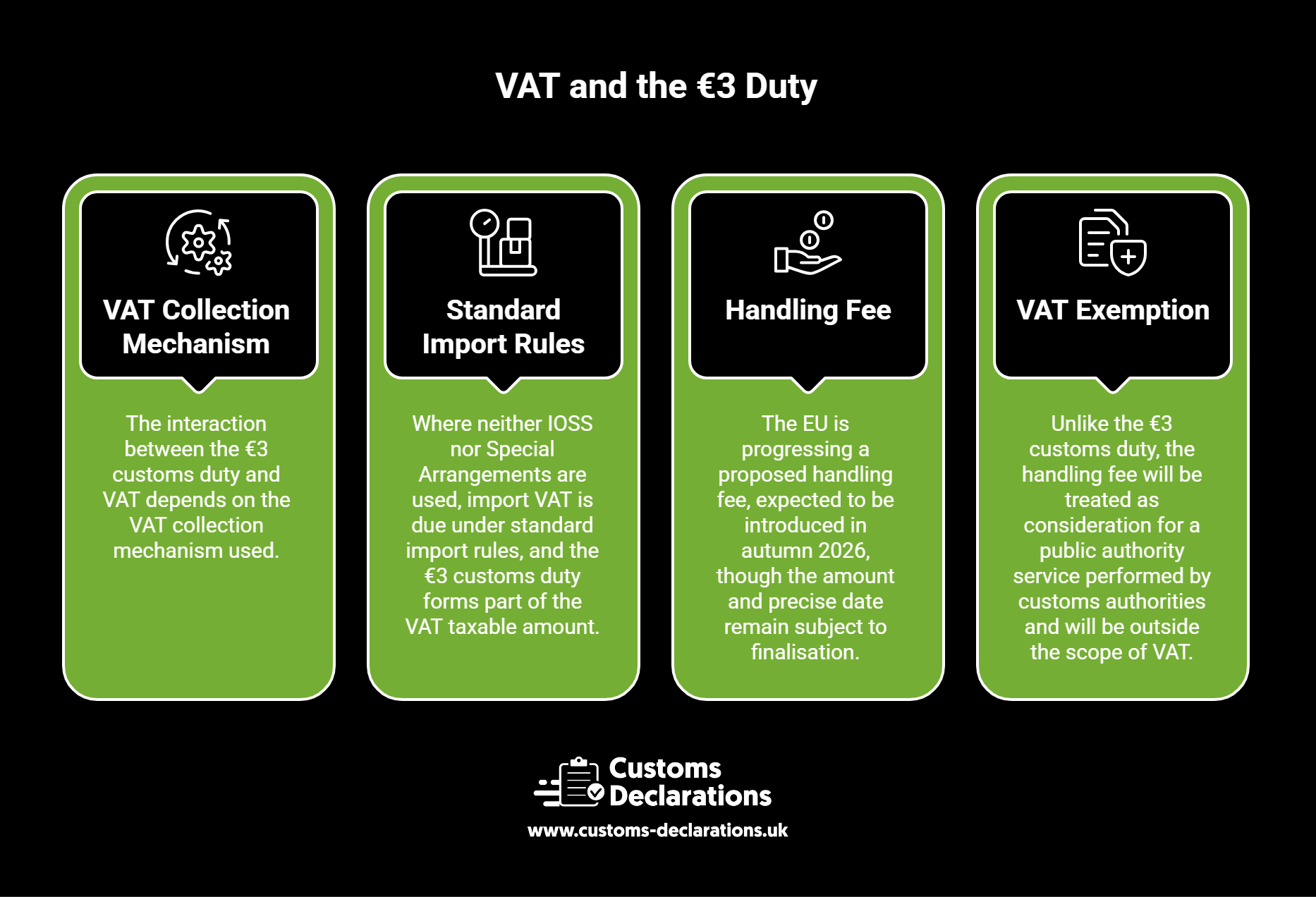

Under Council Regulation (EU) 2026/382, the €3 customs duty becomes payable when the customs declaration for release into free circulation is accepted by customs authorities.

The interaction between the €3 customs duty and VAT depends on the VAT collection mechanism used. Where neither IOSS nor Special Arrangements are used, import VAT is due under standard import rules, and the €3 customs duty forms part of the VAT taxable amount — meaning VAT is charged on the duty itself.

Separately, the EU is progressing a proposed handling fee, expected to be introduced in autumn 2026, though the amount and precise date remain subject to finalisation. Unlike the €3 customs duty, the handling fee will be treated as consideration for a public authority service performed by customs authorities and will be outside the scope of VAT — it will not form part of the VAT taxable amount at importation. Businesses may therefore face both a customs duty that attracts VAT and a handling fee that does not.

Product Identifiers: A New Data Requirement

Alongside the €3 duty, the EU is introducing a new traceability requirement. Product Identifiers (PIDs) will become mandatory from 1 November 2026, though they can be declared on a voluntary basis from 1 July 2026. PIDs will help customs authorities detect and block unsafe or non-compliant goods.

This requirement will affect any business shipping goods to EU consumers that has not previously been required to provide standardised product identification data at declaration level. Sellers using marketplaces should confirm whether the platform, the logistics provider, or the seller bears responsibility for populating PID data in customs declarations.

The Broader Context: A Global Shift Away from De Minimis Exemptions

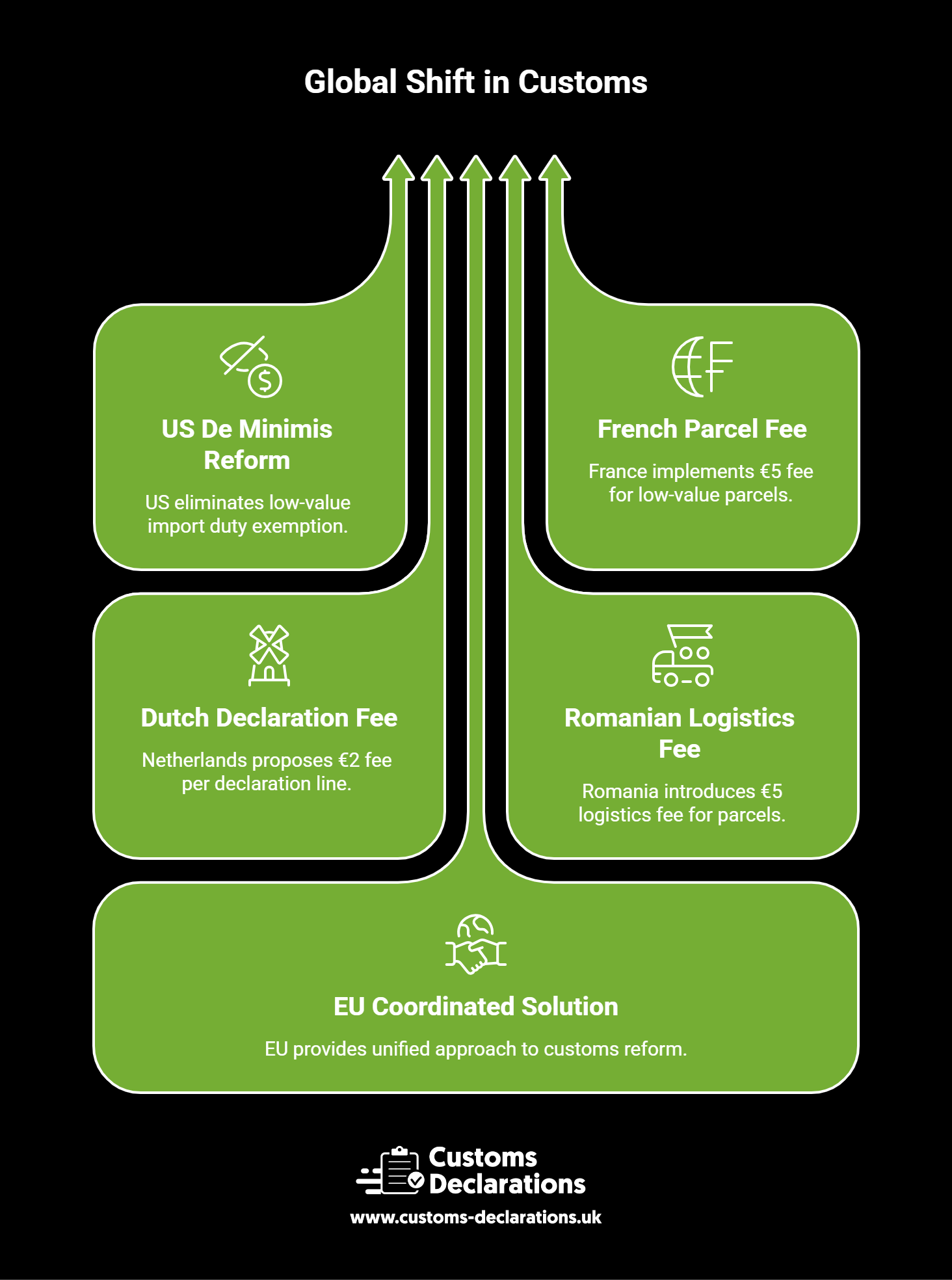

The EU’s reform does not sit in isolation. The United States removed its own low-value import duty exemption in 2025, and the EU’s move is part of the same broad international direction of travel: major economies tightening the treatment of low-value imports, pulling more parcels into formal customs processes with more data and more compliance obligations.

Several EU Member States had already moved independently. France introduced an initial €2 fee for low-value parcels, subsequently raised to €5. The Netherlands proposed a €2 fee per declaration line. Romania introduced a logistics fee of approximately €5. The European Commission was keen to avoid a fragmented, country-by-country approach, and the agreed EU-wide measure provides a coordinated solution during the transition period.

The Commission’s stated objectives for the reform extend beyond revenue. The €3 duty levels the playing field, ensuring that all businesses bringing goods to the EU market — whether buying in bulk or individually — are subject to customs duties and comply with the rules. Product safety, undervaluation fraud, parcel splitting, and the environmental footprint of high-volume parcel logistics are all cited as drivers.

Implications for UK Businesses and Freight Operators

For UK-based businesses selling to EU consumers, the practical impact depends significantly on how goods are sourced and fulfilled.

Businesses that import goods into the EU in bulk — for example through EU fulfilment centres or Amazon FBA — are largely unaffected by the €3 duty, as those goods are already subject to full EU customs procedures on entry. The change does not alter the economics of bulk-then-distribute models.

The picture is more challenging for businesses shipping individual parcels directly to EU consumers from the UK. Each parcel valued under €150 will now attract a €3 duty charge per tariff-classified item. For lower-value products, this charge can represent a meaningful percentage of the item’s price, and at the point of sale this cost must be either absorbed by the seller or passed to the consumer.

For freight forwarders and hauliers, the key operational changes relate to data requirements. Every low-value e-commerce shipment entering the EU now requires accurate HS classification per item, correct customs valuation, and — from November 2026 — compliant product identifiers. Generic descriptions such as “accessories” or “mixed goods” are no longer acceptable under a regime that applies duty per tariff classification.

Businesses operating IOSS registrations should review how their VAT and customs data flows interact under the new rules, in particular where FTA-originating goods are concerned.

The Road to 2028: What Comes Next

By 1 December 2027, the Commission must assess whether a centralised Union IT infrastructure to levy import duties on distance sale consignments will be realistically operational by 1 July 2028. If it determines that the EU Customs Data Hub will not be operational by that date, it may submit a proposal to extend the transitional measure.

Once the Customs Data Hub is operational, the transition from a flat €3 rate to a permanent, classification-based tariff regime will be complete. Low-value e-commerce imports will then be subject to the same tariff treatment as any other import, with duty calculated according to what the goods are and where they originate. Five tariff brackets are currently proposed under the permanent framework.

Customs professionals, freight forwarders, and traders should treat 1 July 2026 not as a final destination but as the beginning of a sustained period of regulatory change. Building robust HS classification processes, accurate customs valuation practices, and compliant declaration data quality now provides the foundation for adapting to the permanent regime in 2028 and beyond.

Conclusion

The €3 flat-rate duty on low-value e-commerce imports marks the end of an era. The de minimis exemption that shaped cross-border e-commerce for decades has closed, and the EU has signalled clearly that the era of duty-free small parcel imports is over. For the 2026–2028 transitional period, the rules are now clear: every item in every consignment valued at €150 or less is subject to a €3 customs duty at the point of EU entry, with the precise charge determined by tariff classification rather than parcel count.

For businesses trading between the UK and the EU — whether as importers, exporters, freight forwarders, or online sellers — the change demands attention to data quality, classification accuracy, and customs declaration processes. Those with robust compliance foundations are well placed to adapt. Those without them face increasing exposure as the EU’s customs modernisation agenda continues to tighten.