How Customs Declarations UK Supports Compliant Trade

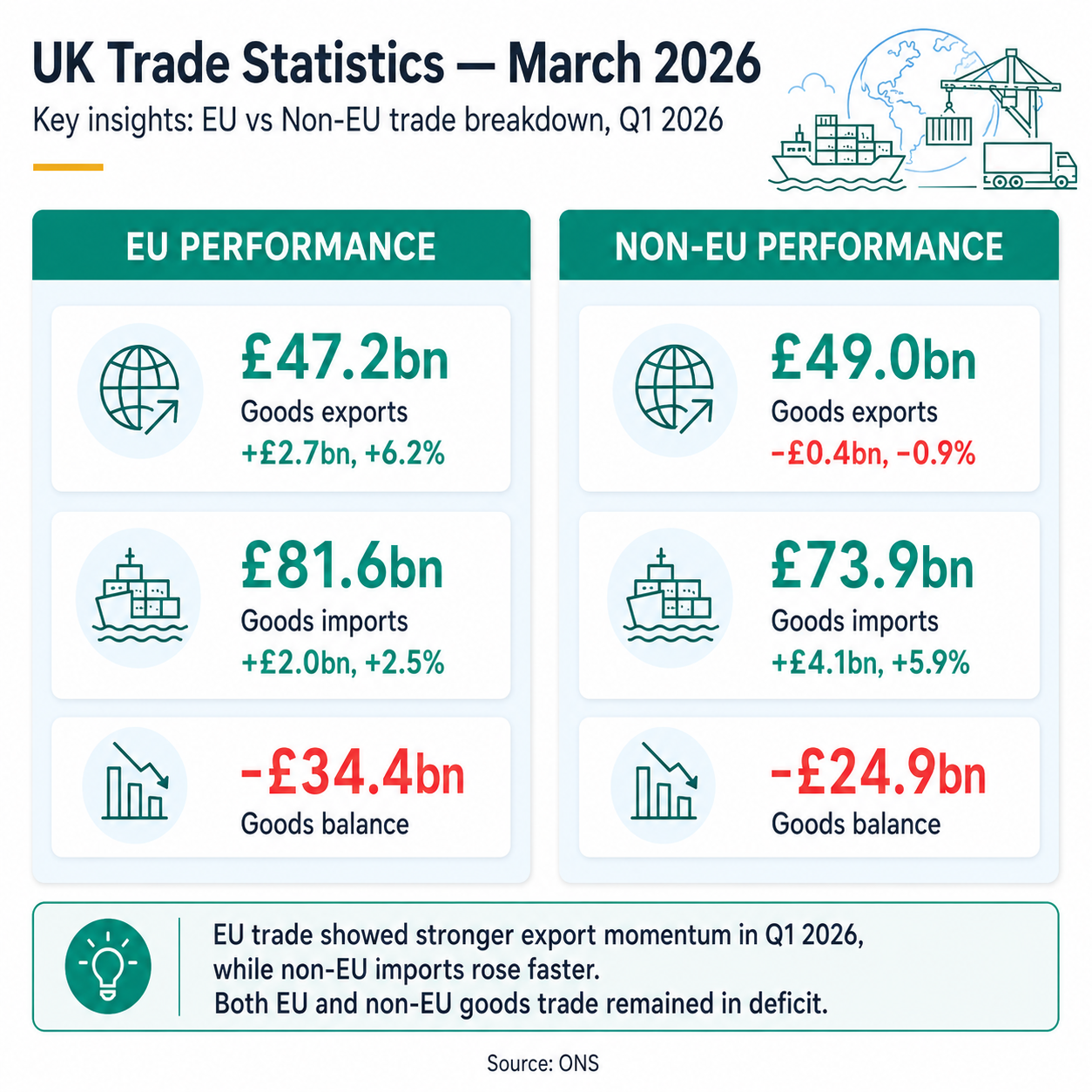

Against the backdrop of rising trade volumes, widening goods deficits, and the commodity complexity evident in the March 2026 data, the ability to file accurate, validated customs declarations efficiently is more important than ever.

The Customs Declarations UK platform provides importers, exporters, freight forwarders, and customs agents with a structured, compliant pathway into HMRC’s Customs Declaration Service. Through guided, plain-English workflows, users can prepare and submit import declarations and export declarations covering the full range of commodity types represented in the ONS trade statistics—from office machinery and fuel products to vehicles, chemicals, and pharmaceutical goods.

For import declarations, the platform supports accurate commodity code entry across Chapters 84 and 85 for machinery, Chapter 87 for vehicles, and energy products across Chapter 27, with real-time validation to detect missing or inconsistent data before submission to CDS. Origin declarations—critical for claiming duty-free treatment on EU goods under the UK-EU Trade and Cooperation Agreement—are captured within the declaration workflow alongside Incoterms, customs value components, and supporting document references.

For ENS safety and security declarations, the platform aligns submission data with carrier filings to prevent the mismatches that are a common cause of avoidable border delays. All accepted declarations and Movement Reference Numbers are archived securely for the statutory six-year retention period, providing the individual business-level audit trail that the HMRC data correction episode highlights as indispensable.

Businesses processing high volumes of declarations—particularly those responding to the import growth patterns evident in Q1 2026—can take advantage of bulk upload functionality via CSV and Excel, reusable templates, and clone functionality for repeat lanes, reducing manual entry burden and improving throughput without sacrificing compliance accuracy.

To learn more about the platform’s capabilities, visit the Customs Declarations UK solutions page or explore the pricing information.