The European Union’s Carbon Border Adjustment Mechanism has transitioned from reporting to full enforcement, marking a fundamental shift in how carbon-intensive goods are imported into the EU. On January 14, 2026, the European Commission activated the “definitive period” of CBAM, requiring customs validation of carbon declarations before goods can be released for free circulation. For UK exporters shipping iron, steel, aluminum, cement, fertilizers, hydrogen, and electricity into EU markets, this regulatory milestone demands immediate operational adjustments to declaration workflows, supplier coordination, and compliance documentation.

The early compliance data demonstrates strong industry response. In the first week of enforcement, over twelve thousand economic operators submitted applications for authorized CBAM declarant status, with more than four thousand already receiving approval. Customs systems successfully validated over ten thousand import declarations covering 1.66 million tonnes of CBAM goods, with iron and steel accounting for ninety-eight percent of validated tonnage. Fertilizers, cement, and aluminum comprised the remainder, while hydrogen and electricity imports are expected to grow as those markets develop.

Understanding CBAM and the enforcement timeline

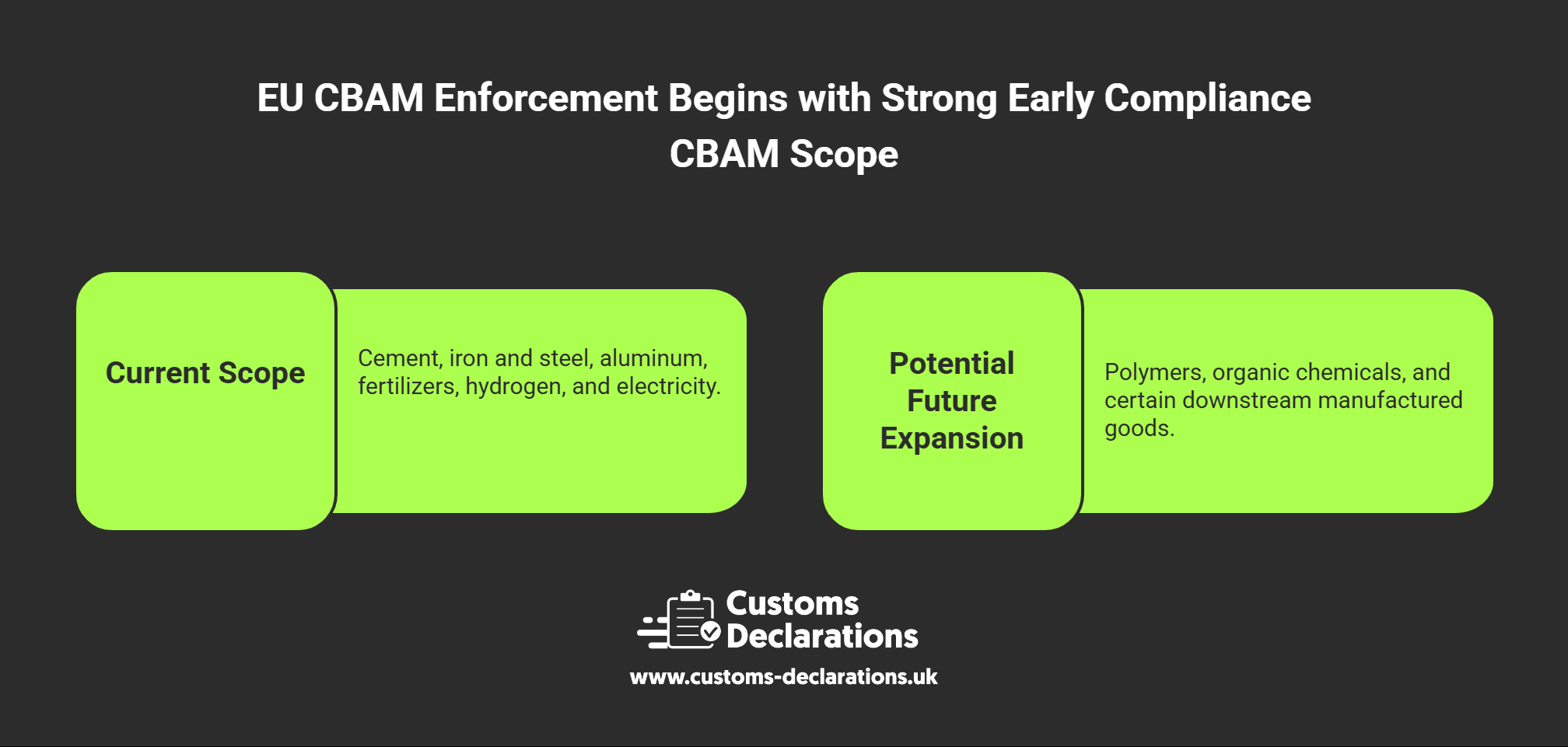

The Carbon Border Adjustment Mechanism is the EU’s policy instrument designed to prevent carbon leakage by imposing a carbon price on imported goods equivalent to what EU producers pay under the Emissions Trading System. The mechanism applies to sectors where carbon leakage risk is highest and where emissions can be measured with reasonable precision. The current scope covers cement, iron and steel, aluminum, fertilizers, hydrogen, and electricity, with potential future expansion to polymers, organic chemicals, and certain downstream manufactured goods.

CBAM implementation began with a transitional reporting period on October 1, 2023, during which importers submitted quarterly emissions reports without facing financial obligations or border enforcement. This phase allowed the Commission to refine methodologies and provided industry with preparation time. The definitive period launched on January 14, 2026, represents full enforcement. Customs authorities in all EU member states now validate CBAM declarations as part of import clearance. Goods covered by CBAM cannot be released for free circulation unless the importer is registered as an authorized CBAM declarant and the customs declaration includes valid CBAM data validated in real time at the border.

Immediate compliance obligations for UK exporters

UK businesses exporting CBAM goods to the EU face immediate compliance requirements spanning registration, emissions data collection, customs declaration preparation, and financial planning. Any business importing CBAM goods into the EU must apply for authorized CBAM declarant status through the CBAM Registry operated by the European Commission. This application requires proof of establishment in the EU or appointment of an indirect customs representative established in an EU member state. UK-based businesses without an EU entity typically appoint an EU customs agent or subsidiary to fulfill this role, adding coordination complexity and cost to the supply chain.

Once authorized, declarants must collect detailed emissions data for each consignment, including direct emissions from the production process, indirect emissions from consumed electricity where applicable, and any precursor emissions embedded in raw materials. The EU provides default values for each product category, but these defaults are intentionally conservative and often result in higher certificate surrender requirements. Importers can reduce compliance costs by obtaining actual emissions data from suppliers, verified according to EU-approved methodologies. This requires suppliers in the UK to implement monitoring systems, calculate emissions according to CBAM rules, and provide verifiable documentation with each shipment.

Customs declarations must now include CBAM-specific data elements. For each line item covered by CBAM, the declaration must reference the CBAM goods category, the quantity in the prescribed unit of measure, the total embedded emissions in tonnes of CO2 equivalent, and the importer’s authorized CBAM declarant number. These data fields are mandatory and validated in real time by customs systems. An incomplete or incorrect CBAM declaration will result in rejection at the border, triggering delays, storage costs, and potential contractual disputes.

Financial planning is equally critical. CBAM certificates are purchased through periodic auctions on the CBAM Registry platform, with prices tracking the EU ETS allowance market. As of January 2026, ETS allowances are trading in the range of seventy to eighty euros per tonne of CO2, though prices fluctuate based on energy market conditions and policy developments. Importers must forecast their annual emissions exposure, purchase certificates in advance to avoid supply shortages, and manage price risk through appropriate hedging or contracting strategies. For a shipment of one thousand tonnes of steel with embedded emissions of two tonnes of CO2 per tonne of product, the CBAM certificate cost at seventy-five euros per tonne of CO2 would be one hundred fifty thousand euros, a material cost that must be absorbed somewhere in the supply chain.

The UK’s position and sector-specific considerations

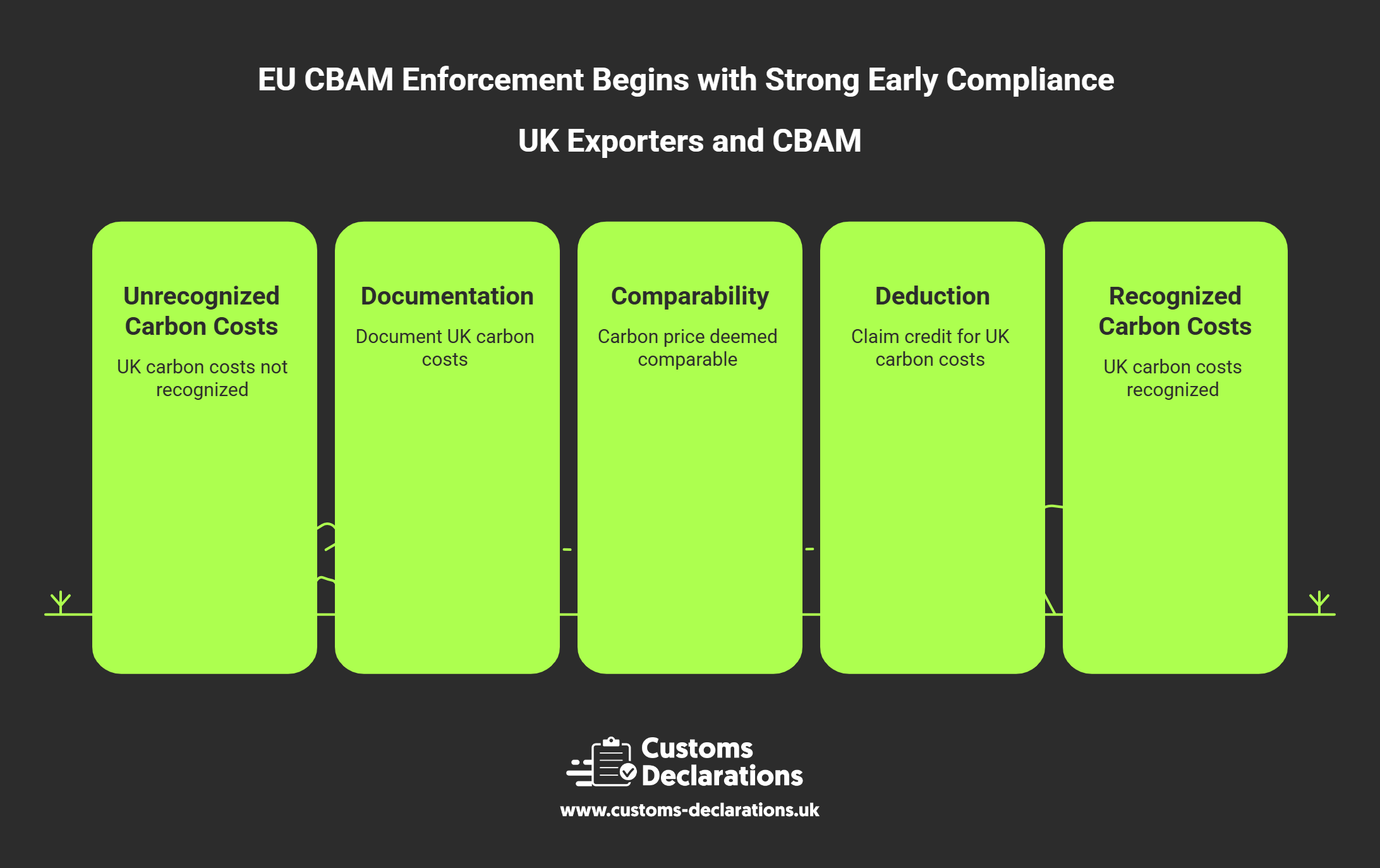

The United Kingdom is not exempt from CBAM. While the UK maintains its own Emissions Trading Scheme with similar objectives to the EU ETS, the European Commission has not granted equivalence recognition that would reduce or eliminate CBAM obligations for UK exports. This means UK exporters face the same CBAM obligations as exporters from any third country. Any carbon costs paid in the UK under the UK ETS may theoretically be deducted from the EU CBAM liability, but only if properly documented and if the carbon price is deemed comparable under CBAM rules. The practical burden of demonstrating this deduction falls on the importer, and many UK exporters are finding it simpler to calculate and surrender CBAM certificates based on full embedded emissions rather than attempting to claim credit for UK carbon costs.

Iron and steel dominate early CBAM enforcement volumes, illustrating both the complexity and materiality of the new regime. Steel production is emissions-intensive, with traditional blast furnace routes generating approximately two tonnes of CO2 per tonne of crude steel, while electric arc furnace routes using scrap inputs produce significantly lower emissions. The embedded emissions in finished steel products depend on the production route, the electricity grid carbon intensity, and the efficiency of the specific facility. UK steel exporters must provide installation-level emissions data to EU importers, covering both direct emissions from iron and steelmaking and indirect emissions from electricity consumption.

The challenge for steel traders and distributors is that they often source from multiple mills and may not have direct visibility into production-level emissions data. In these cases, EU default values apply, which are set conservatively to incentivize accurate reporting. This creates a competitive disadvantage for supply chains with weak data transparency and rewards vertically integrated producers who control emissions information. Aluminum, cement, and fertilizers face similar dynamics but with different technical challenges related to electricity intensity, process emissions, and feedstock sourcing.

Integrating CBAM into customs workflows

CBAM adds a new dimension to customs declarations that requires coordination between commercial, environmental, and logistics teams. Previously, an import declaration for steel might include tariff classification, customs value, origin, and applicable trade preferences. Now, the same declaration must also capture the CBAM goods category code, total embedded emissions, authorized declarant number, and potentially deduction claims for carbon costs already paid. This data must be accurate and must align with supporting documentation held in the importer’s CBAM Registry account.

For businesses using customs software or cloud-based declaration platforms, this means system updates and workflow adjustments. Data fields for CBAM must be added to declaration templates, validation rules must be updated to check for completeness and consistency, and user interfaces must guide declarants through additional input requirements. Coordination with suppliers is equally important. UK exporters should request that suppliers provide a standardized emissions data sheet with each shipment, covering the scope of emissions required under CBAM rules, the calculation methodology used, and any third-party verification. This document becomes part of the commercial package alongside the invoice, packing list, and certificate of origin.

Record-keeping requirements are strict. Importers must retain all emissions documentation, calculation worksheets, supplier attestations, and CBAM certificate purchase records for at least four years. These records are subject to audit by EU customs authorities and by the designated CBAM competent authority in the member state where the importer is established. Audits may examine whether emissions data was calculated correctly, whether deductions for carbon costs paid were justified, and whether the correct number of CBAM certificates were surrendered. Non-compliance can result in penalties, additional certificate surrender requirements, and reputational damage.

Strategic responses and practical steps

The strategic response for many UK businesses is to invest in decarbonization. Lower emissions reduce CBAM costs directly, making UK products more competitive in the EU market. Steelmakers are exploring hydrogen-based direct reduction and electric arc furnace expansion. Cement producers are increasing the use of alternative fuels and supplementary cementitious materials. Aluminum smelters are securing long-term renewable electricity contracts to demonstrate low-carbon credentials. These investments require capital and technical expertise, but they align with both CBAM compliance and broader climate transition goals.

UK businesses exporting CBAM goods to the EU should take immediate action to ensure compliance and minimize commercial disruption. Confirm product scope by reviewing your export portfolio against CBAM goods categories and identifying which items are covered. For each covered product, determine the applicable emissions calculation methodology and identify required data sources. Engage with EU customers or customs representatives to confirm their authorized CBAM declarant status and agree on the format and timing of emissions data provision. Many EU importers are establishing standard data templates that align with their internal systems and customs software.

Invest in internal systems and training to capture and report emissions data accurately. This may involve upgrading production monitoring systems, implementing carbon accounting software, or training staff on CBAM calculation methodologies. Review customs declaration workflows to incorporate CBAM data fields, and coordinate with freight forwarders, customs brokers, and EU agents to ensure that everyone in the supply chain understands their role in CBAM compliance. Monitor certificate requirements and manage purchases proactively, establishing a purchasing strategy that aligns with actual import volumes and manages price volatility. Maintain comprehensive records, documenting every emissions calculation, supplier attestation, certificate purchase, and customs declaration in organized digital systems with search and retrieval capabilities.

Conclusion

The activation of CBAM enforcement on January 14, 2026 represents a permanent shift in the regulatory landscape for UK-EU trade in carbon-intensive goods. The early compliance data demonstrates that industry is responding, with thousands of businesses obtaining authorized declarant status and customs systems processing validated declarations at scale. However, the administrative burden is substantial, and the financial cost of CBAM certificates is material. UK exporters who invest in accurate emissions measurement, robust data management, and streamlined customs workflows will find themselves better positioned to compete in the EU market. CBAM is live enforcement at the border with real financial and operational consequences, and businesses that treat compliance as a strategic priority will navigate this transition most successfully.