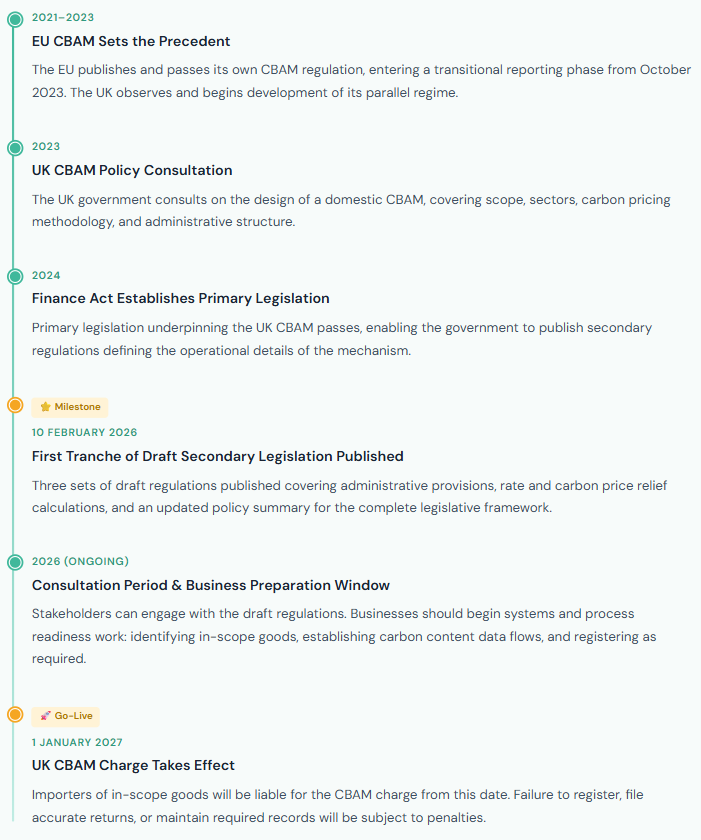

On 10 February 2026, the UK government published the first tranche of draft secondary legislation for the UK Carbon Border Adjustment Mechanism (CBAM), marking a pivotal step toward one of the most significant trade policy shifts since Brexit. The mechanism is scheduled to take effect on 1 January 2027, giving importers less than a year to prepare.

For businesses importing carbon-intensive goods into Great Britain, this is not a distant regulatory abstraction. It is an imminent compliance obligation with real cost implications, new registration requirements, and substantial record-keeping duties. Understanding the framework — and acting early — is the difference between a smooth transition and a disruptive scramble.

💡 What is the UK CBAM?The Carbon Border Adjustment Mechanism is a carbon pricing instrument that applies to imports of specific carbon-intensive goods entering the UK. Its purpose is to prevent “carbon leakage” — the risk that UK businesses shift production abroad to avoid domestic carbon costs, only to import those same goods back without any carbon price attached. In practical terms, importers of in-scope goods will pay a charge that reflects the carbon price that would have been paid had those goods been produced under UK domestic carbon pricing rules. The charge is based on the embedded carbon content of the imported goods and the prevailing UK Emissions Trading Scheme (ETS) carbon price. |

| ⚠️ Reporting obligations begin before the charge does Businesses are likely to face data collection and registration requirements in advance of the 1 January 2027 charge date. Early engagement with the CBAM framework is strongly advised — waiting until launch day will not be feasible for most importers. |

The February 2026 publication comprises three distinct instruments. Together, they form the administrative and financial backbone of the UK CBAM. Click each to explore what it covers.

This regulation establishes the procedural framework businesses must follow. It is the most operationally significant instrument for importers, as it directly dictates the compliance steps required before and after the CBAM charge applies.

This regulation addresses the financial mechanics of CBAM: how the charge is calculated and under what circumstances it can be reduced. This is the instrument that will most directly affect landed cost planning and financial modelling for procurement teams.

The updated policy summary accompanies the two statutory instruments and provides a narrative explanation of how the full legislative framework operates as a coherent system. It is the primary document for businesses seeking to understand the policy intent behind the technical rules.

The summary covers the complete regime arc: from scope determination and registration, through to return filing, carbon price calculation, and the audit and enforcement powers available to HMRC. It also explains the government’s intentions around future sector expansion and interaction with the UK ETS reform roadmap.

Importers and their customs teams should treat this document as essential reading alongside the two statutory instruments.

ℹ️ These are draft regulations — consultation is openThe February 2026 publication represents draft secondary legislation, not final law. Businesses have the opportunity to engage with the consultation process and provide feedback on the administrative and financial provisions before they are finalised. |

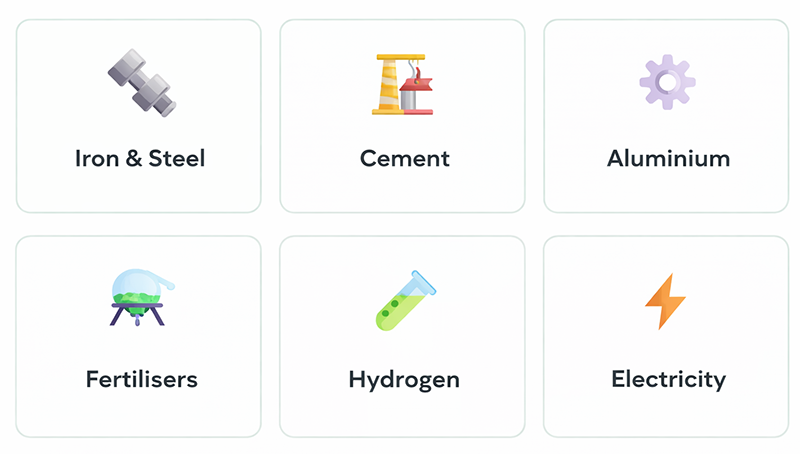

The UK CBAM initially applies to imports of carbon-intensive goods in the following sectors. If your supply chain includes any of these, your business is likely to have CBAM obligations from 1 January 2027. Sector coverage aligns broadly with the EU CBAM, though specific commodity codes and thresholds may differ. Businesses should verify in-scope status against the final published regulations and HMRC guidance.

Businesses importing in-scope goods must register with HMRC under the CBAM regime. This is a separate registration to your existing EORI or VAT registration and will carry its own reference number and account structure.

Registration is expected to be required before the first importation of in-scope goods after 1 January 2027. Businesses should not wait until the charge goes live — HMRC is likely to open a registration window in advance, and early registration will be essential for administrative readiness.

The CBAM charge represents an additional cost of importation that must be incorporated into landed cost calculations alongside customs duty, import VAT, freight, and insurance. For carbon-intensive goods with high embedded emissions, the CBAM charge could be material.

Procurement and finance teams should begin modelling the CBAM cost under different scenarios: high and low ETS carbon price assumptions, with and without carbon price relief from origin countries, and using both default and actual embedded carbon values. This analysis will inform sourcing strategy and contract negotiations.

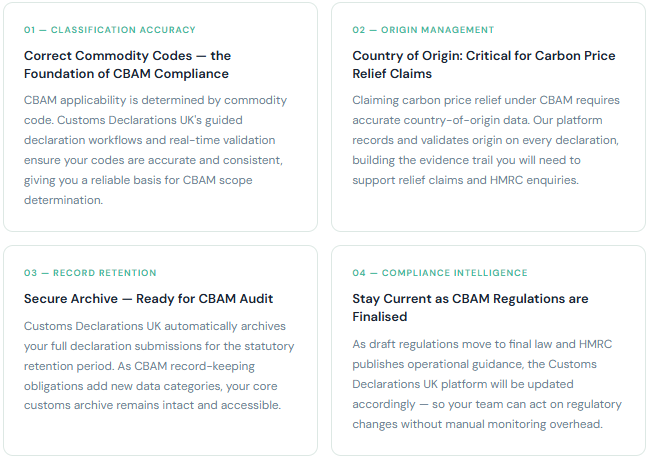

The CBAM administrative provisions include record-keeping obligations that go beyond standard customs declaration retention. Importers will need to maintain evidence of the carbon content of their goods, the basis on which any carbon price relief was claimed, and the methodology used to calculate weight for CBAM purposes.

This documentation should be retained alongside your existing six-year customs record archive. Integrating CBAM records into your existing declaration management system — rather than maintaining a separate, disconnected set of files — will materially simplify future HMRC audits.

Businesses trading with both the EU and the UK face a dual CBAM compliance landscape. While the two mechanisms share common design principles — embedded carbon basis, carbon price relief for origin-country pricing, sector alignment — they are distinct legal regimes with separate registration, reporting, and return obligations.

A key strategic consideration is whether carbon content data collected for EU CBAM purposes can be reused for UK CBAM compliance. In practice, much of the underlying supplier data should be transferable, but the precise methodologies and default values differ. Early engagement with both regimes in parallel is strongly advisable for businesses affected by both.

While the CBAM charge is a new obligation, it sits squarely within the broader customs compliance ecosystem that Customs Declarations UK already supports. Businesses that manage their customs declarations accurately and efficiently today are inherently better positioned for CBAM compliance tomorrow.

🔗 File your import declarations today on Customs Declarations UKManaging your customs declarations through a validated, CDS-integrated platform ensures your commodity codes, origin data, and valuation are accurate and audit-ready — the same foundations CBAM compliance will demand. Visit customs-declarations.uk to explore the platform and get started. |

We value your feedback, and if you have any comments, suggestions or anything else that you would like to highlight to us, we will be delighted to hear from you and incorporate your feedback into our content.

Note: While we have made every attempt to ensure that the information contained in this Site has been obtained from reliable sources, Customs Declarations UK is not responsible for any errors or omissions, or for the results obtained from the use of this information. All information in this Site is provided “as is”, with no guarantee of completeness, accuracy, timeliness or of the results obtained from the use of this information, and without warranty of any kind, express or implied, including, but not limited to warranties of performance, merchantability and fitness for a particular purpose. Nothing herein shall to any extent substitute for the independent investigations and the sound technical and business judgment of the reader. In no event will Customs Declarations UK, or its partners, employees or agents, be liable to you or anyone else for any decision made or action taken in reliance on the information in this Site or for any consequential, special or similar damages, even if advised of the possibility of such damages. Certain links in this Site connect to other Web Sites maintained by third parties over whom Customs Declarations UK has no control. Customs Declarations UK makes no representations as to the accuracy or any other aspect of information contained in other Web Sites.