7. Filing Customs Declarations with Customs Declarations UK

Filing a CDS declaration for organic food imports from France is a structured process that requires accuracy across all data elements. The Customs Declarations UK platform provides importers with a guided, validated pathway into HMRC’s Customs Declaration Service, making this process accessible and audit-ready even for businesses managing declarations in-house without specialist customs staff.

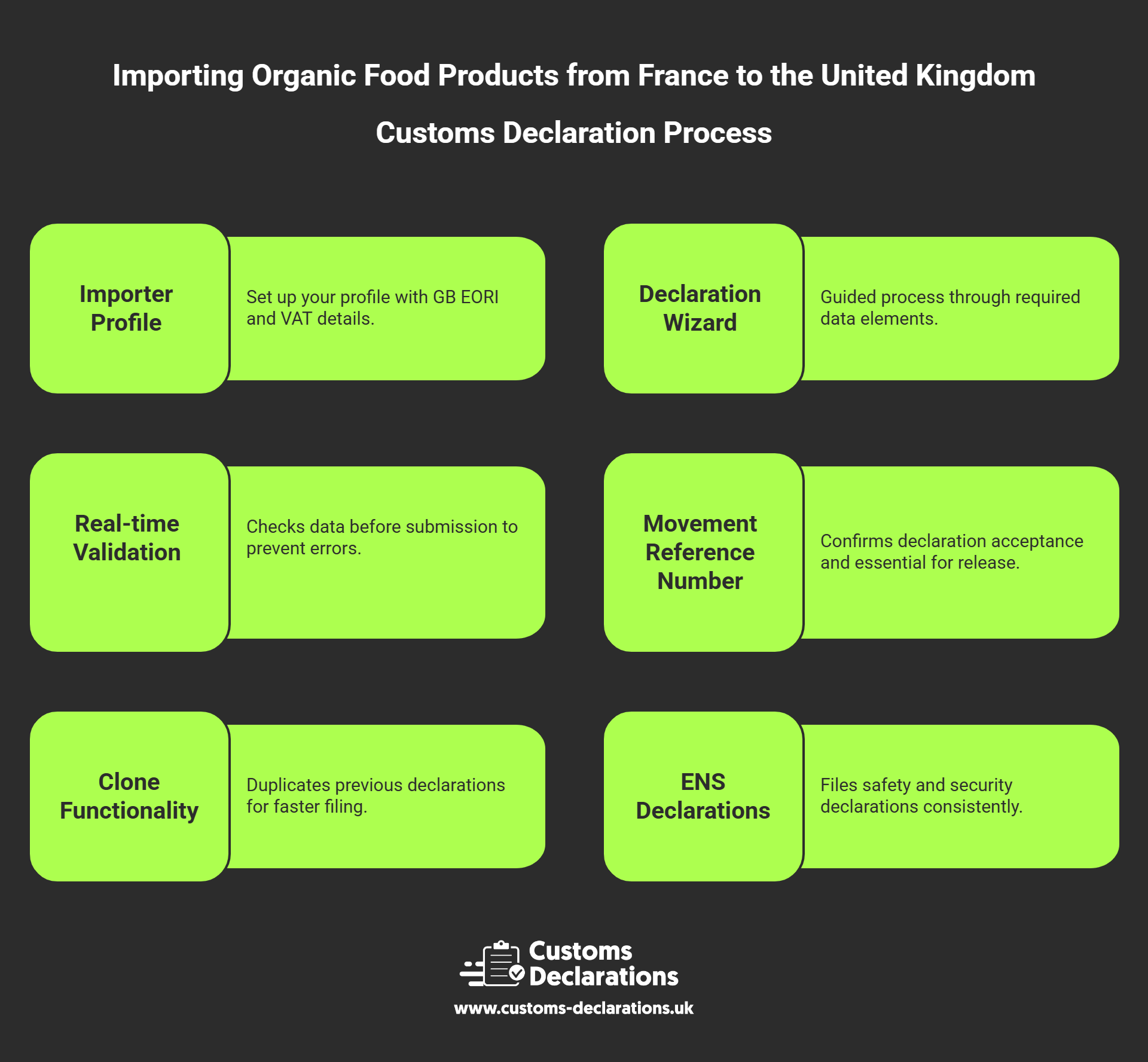

Within the platform, importers begin by setting up their importer profile, including their GB EORI number and VAT registration details. These are reused across all declarations, eliminating repetitive data entry. When creating a new import declaration for a shipment of French organic food, the wizard guides the user through each required data element: the commodity code, the commercial description of the goods, the customs value and its components, the Incoterms agreed with the French supplier, the country of origin, and the preference claim under the TCA where applicable.

One of the most valuable features for organic food importers is the real-time validation engine, which checks each data element before the declaration is transmitted to HMRC. Common errors—such as mismatches between declared values and invoice totals, missing supporting document references, or incomplete party identifiers—are flagged at the point of entry rather than after submission, preventing rejections that cause border delays. For organic imports specifically, the IPAFFS pre-notification reference can be recorded in the relevant documentary field, ensuring that the declaration and the health control notification are aligned.

Upon acceptance by HMRC, Customs Declarations UK platform immediately returns the Movement Reference Number (MRN), which confirms that the declaration has been lodged and accepted. This number is essential for port release procedures and must be shared with the freight forwarder and carrier. The full declaration record is then archived securely within the platform for the statutory six-year retention period, providing a single, accessible source of truth for any subsequent HMRC audit or market surveillance enquiry.

For importers managing multiple regular lanes—such as weekly shipments of organic produce from a consistent French supplier— Customs Declarations UK platform’s clone functionality allows a previously accepted declaration to be duplicated and updated, dramatically reducing the time required to prepare each new filing. Combined with bulk data upload capabilities for high-volume operators, this makes the platform well suited to the operational rhythm of businesses importing organic food at commercial scale.

Additionally, where safety and security ENS declarations are required—as is the case for certain movements into GB ports operating under the GVMS regime—the platform allows these to be filed consistently with the import declaration data, reducing the risk of mismatches between the carrier’s safety and security filing and the customs entry that are a frequent cause of avoidable holds at the border.