For years, the customs compliance conversation in the UK trade and logistics sector has focused on getting goods across the border. Declarations filed, duties paid, paperwork stamped — job done. But a quiet and significant shift is under way. HMRC and French customs authorities are increasingly turning their attention not just to what happens at the border, but to what happened before and after it. Post-clearance audits are no longer a peripheral concern for large multinationals. They are becoming a very real operational risk for hauliers, freight forwarders, and importers of all sizes — particularly in the wake of mandatory ELO enforcement, which came into full effect on 20 April 2026.

If your business moves freight between the UK and France, the question is no longer simply whether you have the right documents. The question is whether those documents are accurate, complete, consistent — and retrievable months or even years after the truck crossed the Channel.

What Is a Post-Clearance Audit — and Why Does It Matter Now?

A post-clearance audit (PCA) is an examination by a customs authority of an economic operator’s commercial records, transport documents, customs declarations, and related data — conducted after goods have been released. In the UK, HMRC has long held the legal right to conduct these checks under the Customs and Excise Management Act 1979 and subsequent legislation. The EU equivalent powers exist under the Union Customs Code (UCC), Article 48.

In practice, PCAs have historically been most common in high-volume import/export sectors such as retail, pharmaceuticals, and automotive. But the digitalisation of border processes is changing the risk landscape substantially. The introduction of ICS2 (Import Control System 2) and the mandatory ELO system means that customs authorities now hold far richer, more structured data about every crossing than they ever did under legacy systems. That data is timestamped, cross-referenced, and stored — creating a detailed digital audit trail that authorities can interrogate long after the crossing has taken place.

Put simply: the digital footprint left by modern customs processes has made post-clearance auditing significantly easier, more targeted, and more likely to uncover discrepancies.

The ELO as an Audit Trigger

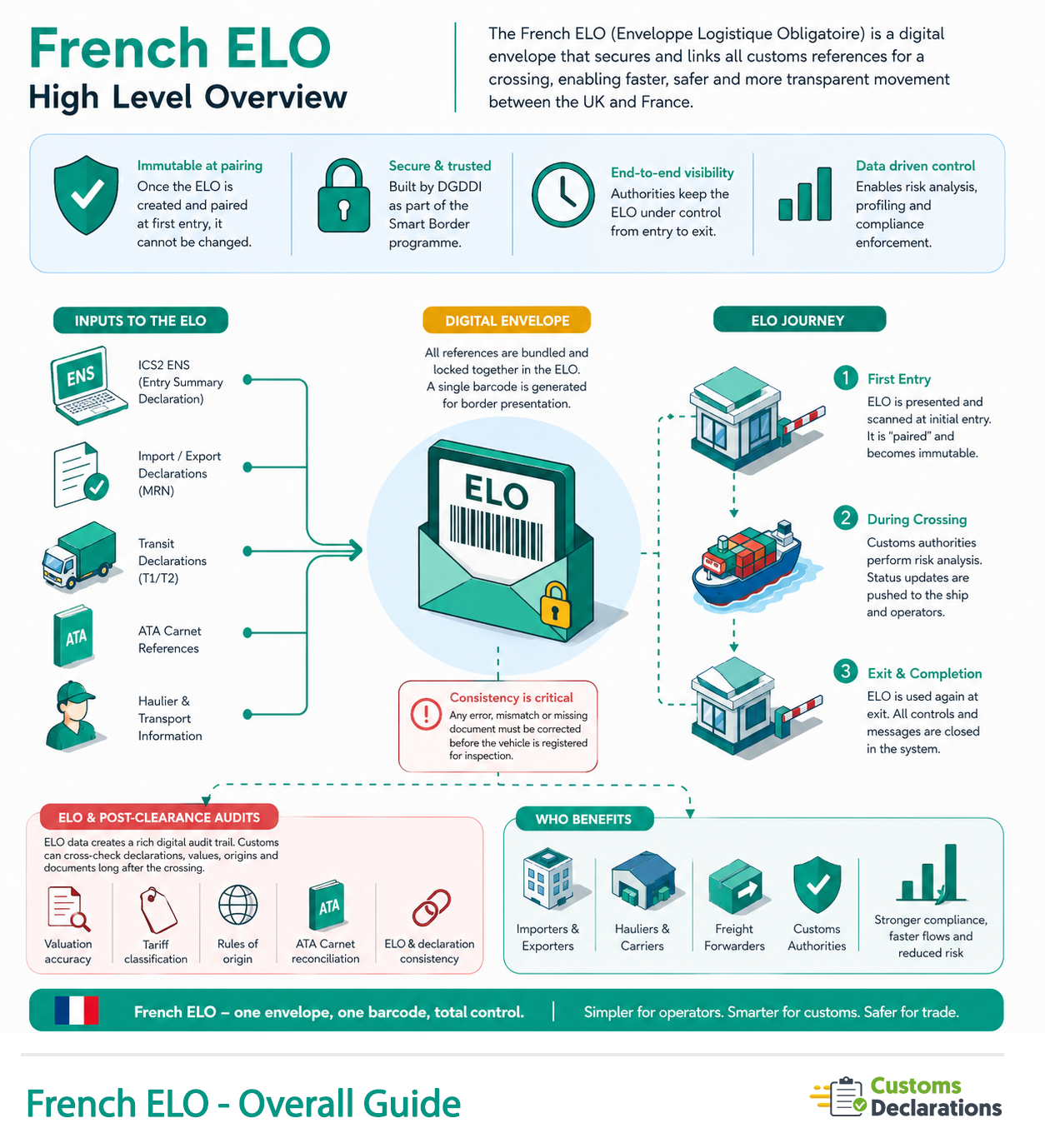

The ELO was introduced by France’s Directorate General of Customs and Indirect Taxes (DGDDI) as part of the Smart Border (SI Brexit) system. It functions as a digital envelope that bundles all customs references for a given crossing — import or export MRNs, ICS2 ENS Movement Reference Numbers, transit documents, ATA Carnet references, and haulier details — into a single, scannable barcode presented at the terminal check-in.

One of the most consequential technical features of the ELO is a principle that DGDDI describes as “immutable at pairing”: once the ELO barcode is scanned at the initial entry check, the envelope and all its associated declarations are locked. No amendments can be made. Any error, inconsistency, or missing document must be identified and corrected before the vehicle is registered for inspection — not after.

This creates an important compliance dynamic. Every ELO that contains errors, mismatched MRNs, or incorrect commodity descriptions is a data point in DGDDI’s system. Over time, patterns of non-compliance build profiles. Operators whose ELOs consistently contain anomalies — even if goods are ultimately cleared — become candidates for more intensive scrutiny, including formal post-clearance audit.

The same logic applies on the UK side through GVMS (the Goods Vehicle Movement Service) and HMRC’s own data infrastructure. The introduction of safety and security declarations for EU imports into Great Britain, which became mandatory from January 2025, means HMRC is now collecting advance cargo data at scale. That data sits alongside customs declaration records, duty payment histories, and EORI-linked trade profiles — a rich dataset from which risk profiles can be constructed.

What Auditors Are Looking For

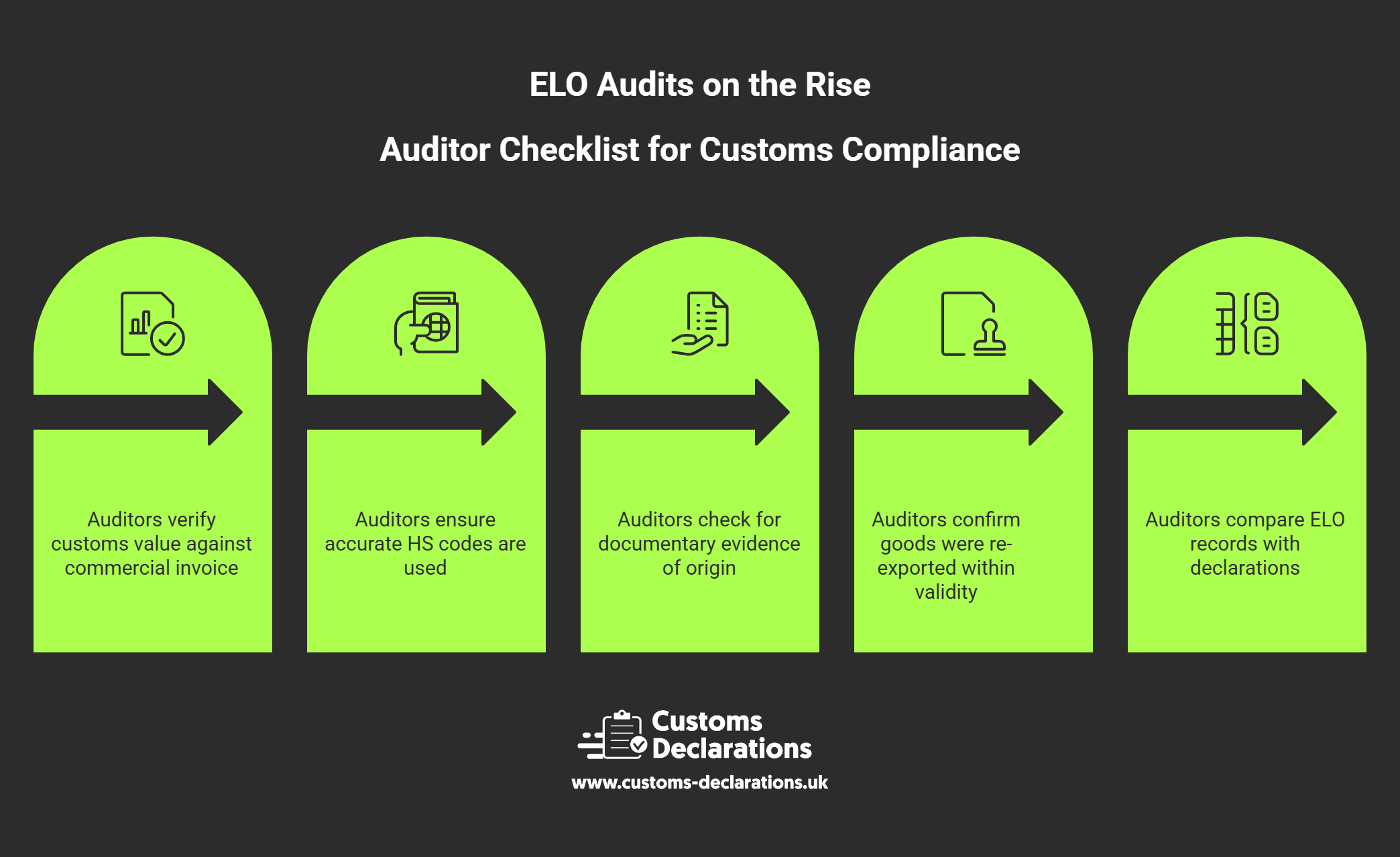

When customs authorities conduct a post-clearance audit in the context of UK–France freight movements, they are typically examining several key areas:

Valuation accuracy. Is the customs value declared consistent with the commercial invoice and the actual transaction value? Undervaluation — whether deliberate or the result of poor recordkeeping — is one of the most common audit findings.

Tariff classification. Are the commodity codes (HS codes) used in customs declarations and ICS2 ENS filings accurate and consistent? A mismatch between the ENS filing and the import declaration is an immediate red flag.

Rules of origin compliance. For goods claiming preferential tariff treatment under the UK–EU Trade and Cooperation Agreement, are the origin declarations supported by documentary evidence? Auditors will want to see supplier declarations, long-term supplier declarations, or movement certificates, not just a claim on the commercial invoice.

ATA Carnet reconciliation. For temporary movements under ATA Carnet — an area of growing relevance given the ELO’s explicit accommodation of carnet-based movements — auditors will check that goods were re-exported within the carnet’s validity period, that all counterfoils were correctly endorsed, and that no permanent import occurred without duty payment.

ELO and declaration consistency. With the ELO now generating a structured digital record of every crossing, auditors can directly compare the ELO’s referenced declarations against the declarations themselves. Any discrepancy — a different consignee, a mismatched MRN, a commodity description that doesn’t align — will be examined.

The ATA Carnet Dimension

The inclusion of ATA Carnets within the ELO framework has added a new layer of compliance complexity for businesses that rely on temporary admission for exhibitions, professional equipment, and commercial samples. The carnet itself remains a valid customs document — it replaces the standard export and import entries for temporary movements — but it must now be referenced correctly within the ELO.

Critically, a customs endorsement is mandatory at each border crossing. Failure to obtain the correct endorsement, or to re-export goods within the carnet’s validity period, creates a duty liability that can surface during a post-clearance audit years after the movement took place. Businesses using ATA Carnets should ensure their internal records are comprehensive: departure dates, endorsement stamps, re-importation records, and the carnet’s correspondence with the ELO reference should all be retained and reconcilable.

Building a Post-Clearance Audit Defence

The most effective defence against an adverse post-clearance audit outcome is not luck — it is systematic recordkeeping and process discipline. Customs authorities are required to give notice of a formal audit, but the records they will want to examine can span five to seven years of commercial activity.

Businesses should ensure they retain:

- All customs declarations (import, export, transit) and their corresponding MRNs

- Commercial invoices, packing lists, and contracts of sale

- ELO barcodes and associated ENS MRN references

- ATA Carnet counterfoils and re-exportation records

- Evidence supporting tariff classification decisions

- Supplier declarations and origin documentation

- CMR consignment notes and transport contracts

The digitisation of ELO and ICS2 records means that customs authorities will likely have better access to a structured record of your crossings than you do — unless your own systems are equally rigorous.

How Customs Declaration UK Can Help

Navigating the combined demands of ELO compliance, ICS2 ENS filings, and post-clearance audit readiness is operationally complex — particularly for businesses that move goods across multiple modes of transport and across different regulatory regimes.

Customs Declaration UK offers a comprehensive, end-to-end declarations service designed to take that complexity off your plate. Whether your freight travels by road through the Channel Tunnel or Calais, by short-sea ferry, by air freight, or by rail, our service covers every mode of transport under a single, consistent compliance framework.

Our specialists handle the full sequence of cross-Channel documentation — from ICS2 ENS filing and MRN generation through to ELO creation and GMR management on the UK side — ensuring that your crossings are not only compliant at the border, but defensible under post-clearance scrutiny. For ATA Carnet movements, we ensure the carnet is correctly referenced within the ELO and that your re-exportation records are structured and retained in a way that withstands audit examination.

The result is a seamless, paperless process for your drivers and logistics teams, with the confidence that every declaration has been completed accurately, every MRN has been correctly cross-referenced, and every document is retrievable when it matters most. In an environment where HMRC and DGDDI are investing in data-driven audit targeting, accuracy at the point of declaration is your most valuable insurance policy — and that is precisely what Customs Declaration UK delivers.

Conclusion: Compliance Doesn’t End at the Border

The mandatory ELO has fundamentally changed what it means to be customs compliant on UK–France freight movements. The border crossing is no longer the end of the compliance journey — it is the beginning of a data record that customs authorities can interrogate for years to come.

Post-clearance audits are rising because the data infrastructure now exists to make them targeted, efficient, and productive. Businesses that treat each crossing as a discrete event — declared, cleared, forgotten — are building a compliance gap that will eventually be exposed.

Those who treat every declaration as a permanent record, every MRN as a traceable reference, and every document as a future audit exhibit are far better placed. In the age of the Smart Border, post-clearance readiness is not an optional extra. It is the new baseline for operating in the UK–France freight corridor — and the businesses that recognise this earliest will carry the least risk.