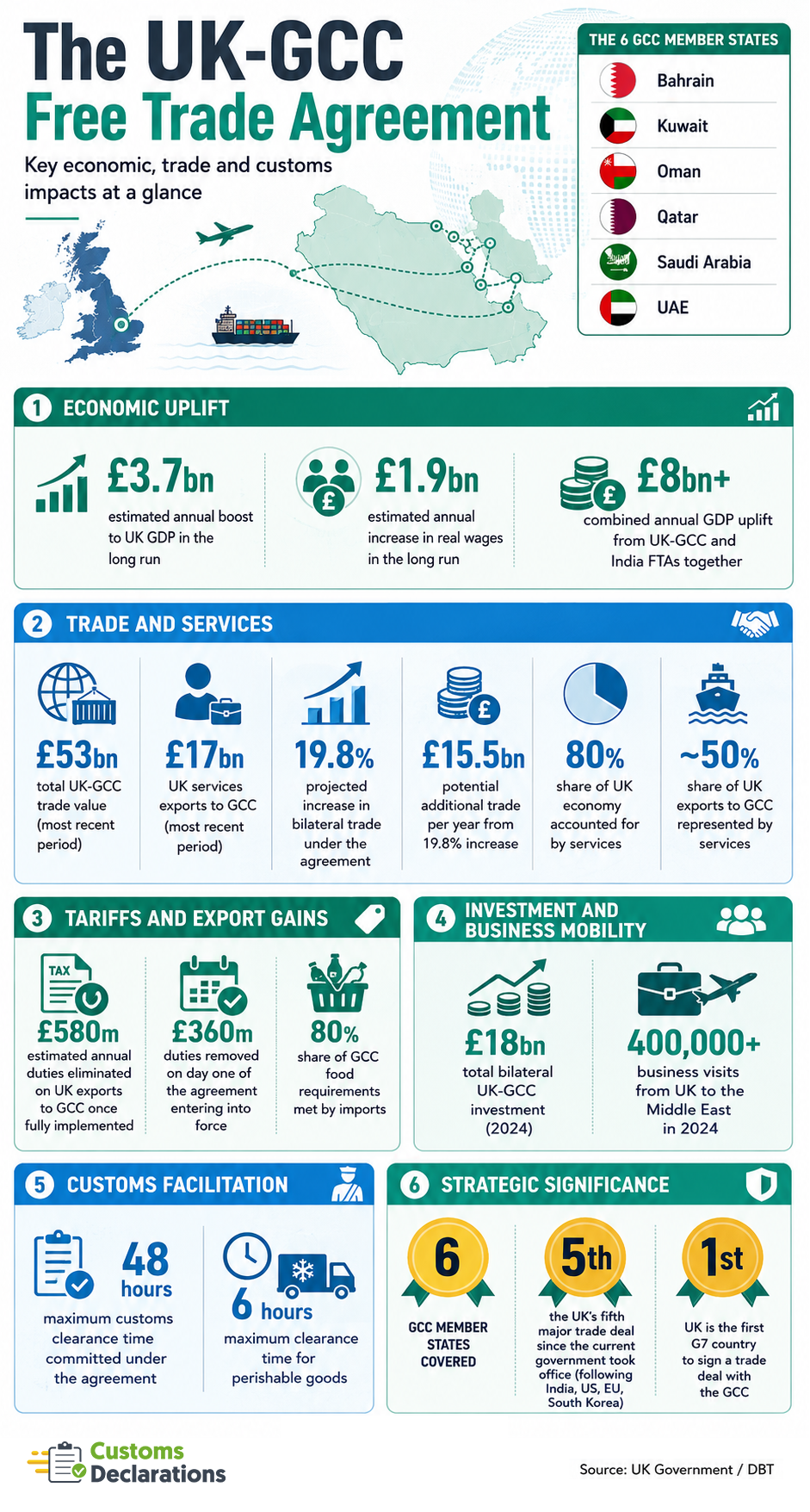

On 20 May 2026, the United Kingdom concluded a landmark Free Trade Agreement with the Gulf Cooperation Council, becoming the first G7 nation to secure such a deal with the six-nation bloc. The agreement covers Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates, and represents a significant realignment of the UK’s post-Brexit trade architecture. For businesses that import or export between the UK and the Gulf, this agreement carries immediate and long-term consequences for duty planning, customs declaration workflows, and documentary compliance.

What the UK-GCC FTA Is and Why It Matters

The Gulf Cooperation Council collectively forms one of the most commercially active regions in the world. Total UK-GCC trade was worth £53 billion and services exports alone reached £17 billion in the most recent period. The new agreement is expected to build substantially on that foundation. Bilateral trade could increase by 19.8%, potentially adding an extra £15.5 billion a year, according to DBT modelling.

For UK businesses, the headline benefit is the removal of tariff costs that have historically made Gulf market entry less competitive. The deal will eliminate duties worth an estimated £580 million a year on UK goods exported to the GCC based on existing trade once fully implemented, with £360 million of that removed on day one of the agreement entering into force.

Beyond tariffs, the agreement is notable for its scope across goods, services, digital trade, and investment. It includes the most ambitious commitments on customs procedures the GCC has ever signed up to, with customs cleared within 48 hours and perishable goods released in under six hours once all requirements are met.

The Customs and Declaration Implications

Free trade agreements do not simplify customs declarations; in several respects, they make the documentation requirements more demanding. To benefit from preferential duty rates, exporters must be able to prove that their goods qualify as originating under the agreement’s rules of origin. This is not a passive entitlement — it requires active evidence gathering, supplier attestations, and declaration-level accuracy.

Businesses that have previously exported to Gulf states under standard Most-Favoured-Nation terms will need to assess whether their products meet the product-specific rules of origin set out in the agreement. Where they do, exporters must obtain or issue the appropriate proof of origin — whether a statement on origin or another qualifying document — and ensure this is referenced correctly in the customs export declaration. On the import side, Gulf-origin goods entering the UK under preference will similarly require verified origin documentation to substantiate any duty relief claimed.

The agreement also introduces new expectations around customs data quality. It includes first-of-its-kind GCC commitments on the free flow of data, signalling that digital trade infrastructure and compliant data practices will increasingly underpin the day-to-day movement of goods.

Businesses should also note the provisions on business mobility. In 2024 there were over 400,000 business visits made from the UK to the Middle East, and the deal will help British professionals including lawyers, engineers, and consultants to travel more easily and stay longer in the region. This matters for service exporters, but it also reflects a broader ambition in the agreement to reduce friction for companies with recurring Gulf trading relationships.

Sectors with Immediate Tariff Benefits

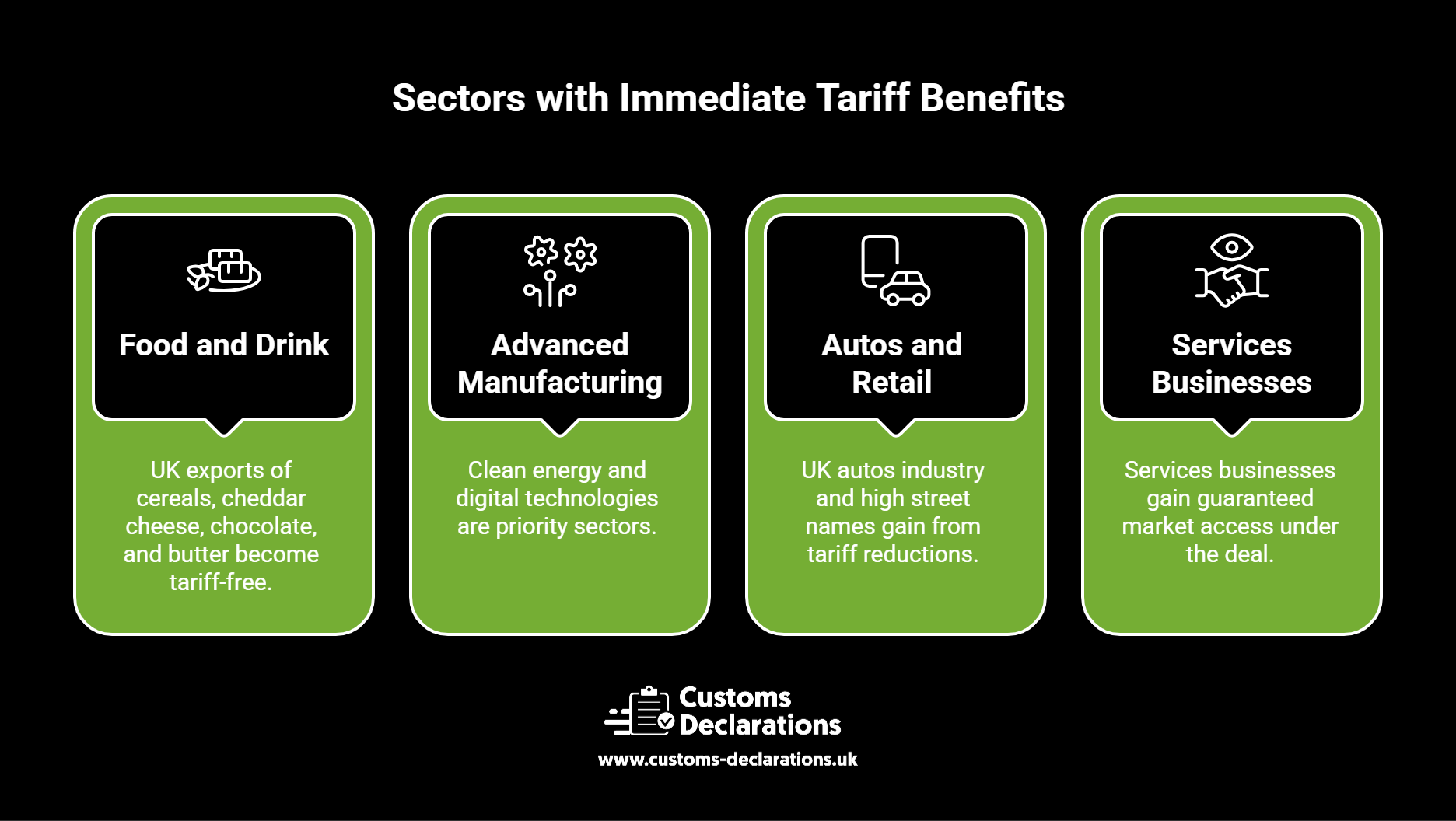

Several sectors are positioned to see direct cost savings from day one of implementation. UK exports of cereals, cheddar cheese, chocolate, and butter are among the goods expected to become tariff-free, supporting British industry to grow. The food and drink sector benefits particularly because the GCC imports over 80% of its food. This creates a structural opportunity for UK producers to compete more aggressively on price in a region that is already highly dependent on imported foodstuffs.

Advanced manufacturing, clean energy, and digital technologies are also cited as priority sectors aligned with the UK’s Industrial Strategy. The UK autos industry alongside high street names like Holland & Barrett stand to gain significantly from the deal, through tariff reductions, stronger intellectual property protections, and simplified customs processes.

For services businesses, which represent the largest share of UK economic output, the picture is similarly positive. UK services account for around 80% of the British economy and around half of UK exports to the GCC, and will gain guaranteed market access under the deal.

Data, Digital Trade, and the Technology Dimension

One of the most forward-looking elements of this agreement is its treatment of digital trade and data. The deal will enable UK companies to store and process data outside the region for the first time ever, which will save businesses money on setting up costly data centres in the Gulf. This has practical implications not only for technology and financial services firms but for any company whose customs, logistics, or compliance platform processes trade data on behalf of Gulf-facing operations. Customs technology providers and cloud-based declaration platforms that serve UK exporters are directly affected by these digital provisions, as they create a more favourable environment for delivering compliant, cross-border digital services.

Trade in Services: A Surplus Under Pressure

Early estimates indicate that exports of services fell by an estimated £0.7 billion (0.5%) in Quarter 1 2026, compared with Quarter 4 2025, because of a £0.7 billion fall in exports of travel services alongside small falls in other service types.

Imports of services remained similar in Quarter 1 2026 compared with the previous quarter, with the largest fall being a £0.7 billion decrease in travel services, offset by a £0.6 billion rise in other business services.

The services surplus of £52.3 billion continues to partially offset the substantial goods deficit of £59.3 billion, resulting in the combined goods and services deficit of £7.0 billion. However, the narrowing services surplus—combined with growing goods imports—represents a structural pressure on the UK’s overall trade position.

For the month of March, exports of services increased by £0.1 billion (0.2%), while imports of services remained similar in value terms. A separate note in the release highlights that the war in Iran affected exports, with new business falling at its fastest rate in nearly a year, and business confidence declining sharply during March.

Investment and the Broader Economic Framework

The agreement reinforces a trading relationship that already extends into substantial two-way investment. Total bilateral investment stood at £18 billion in 2024 and supports critical infrastructure projects including Heathrow Airport. The FTA is designed to protect and grow that investment base by ensuring disputes are resolved fairly and by creating the kind of regulatory certainty that long-term capital commitments require.

When combined with the India trade deal, the UK-GCC and India agreements are estimated together to add over £8 billion a year to UK GDP in the long run when compared to 2040 projections. This framing is important — the GCC agreement does not stand alone; it is part of a sequence of deals that includes India, the United States, the EU, and South Korea, each of which introduces new preference pathways and documentary requirements that customs teams must operationalise.

What Businesses Should Do Now

The practical priority for importers and exporters is preferential origin readiness. Businesses should audit their product portfolios against the GCC rules of origin, identify which goods qualify, and build the supplier documentation processes needed to substantiate preference claims at declaration level. For exporters, this means working with suppliers and manufacturers to obtain clear, accurate statements on origin before shipments move. For importers, it means reviewing whether Gulf-origin goods they bring into the UK are now eligible for duty relief and ensuring their customs broker or declaration platform captures that correctly.

Beyond origin, customs valuation disciplines remain unchanged. The transaction value method continues to apply, and the inclusion of freight, insurance, and other dutiable costs in the declared value is a standing obligation regardless of the preferential tariff rate applied. Accurate valuation protects businesses from post-clearance assessments and maintains the integrity of any preference claim.

The agreement’s commitment to 48-hour clearance and six-hour release for perishables will only be achievable in practice where the underlying customs declarations are complete, accurate, and submitted in advance. This underscores the importance of filing on a compliant, validated platform that performs real-time data checks before submission and aligns safety and security data with the corresponding customs entry.

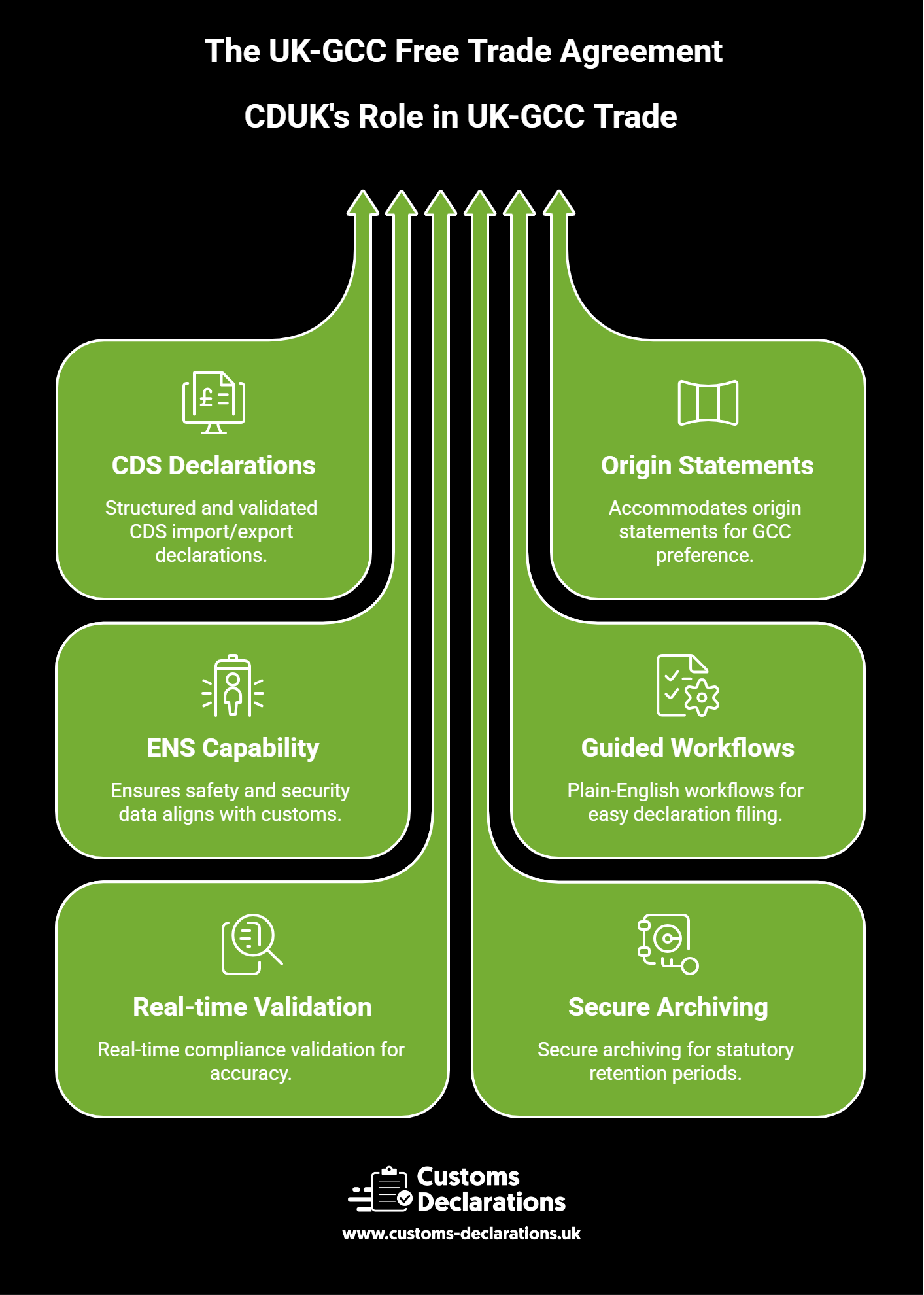

Filing UK-GCC Trade Declarations with Customs Declarations UK

Whether you are exporting goods to Bahrain, importing manufactured equipment from the UAE, or managing repeat movements across multiple GCC markets, the Customs Declarations UK platform provides the structured, validated filing environment that this agreement demands. CDUK supports CDS import and export declarations with guided, plain-English workflows, real-time compliance validation, and secure archiving for the statutory six-year retention period. For exporters claiming GCC preference, CDUK’s declaration workflows accommodate origin statements and preference codes so that the fiscal benefit of the agreement is correctly reflected in every submission. The platform’s ENS capability ensures that safety and security data aligns with customs entries, reducing the risk of holds at the border as trade volumes with the Gulf grow. To explore how CDUK can support your UK-GCC trade operations, visit the Customs Declarations UK platform.